Last updated 7/1/2026

If you have spent decades saving into a 401(k), IRA, or 403(b), and you are now retired or within a few years of it, the question of what Spokane financial advisor to trust with that money carries real weight.

A good decision on Roth conversions, Social Security timing, or how you draw down your accounts can be worth far more than what you pay a financial advisor. A poor decision can quietly cost you for the rest of your life.

That is why choosing a Spokane financial advisor is about much more than finding someone who can pick investments. It is about finding someone who understands retirement income, tax-aware planning, Roth conversions, Social Security, charitable giving, and the specific decisions that show up when your paycheck stops and your savings have to take over.

At Stewardship Concepts Financial Services, we work primarily with Spokane retirees and people nearing retirement. We serve roughly 180 households in Spokane. If you are trying to decide who to trust with your retirement, here are seven questions to ask before you hire anyone.

1. Do they work with people like you?

This is one of the most overlooked questions, and one of the most important.

An advisor can be smart, experienced, and well intentioned and still be the wrong fit for your situation. A young professional building wealth has very different needs than a Spokane couple five years from retirement with $1 million in a 401(k). A retired Avista or Providence employee deciding how to turn savings into income has different needs than a business owner mid-career.

So ask directly:

- Do you regularly work with retirees and people nearing retirement?

- Do you work with clients who have large 401(k), IRA, or 403(b) balances?

- Do you help people think through Roth conversions, Social Security, Medicare, and tax-aware withdrawals?

The closer you are to retirement, the more this matters. You do not just need an investment account. You need a coordinated plan.

2. Are they retirement-focused or more general?

A lot of advisors call themselves comprehensive planners. That phrase can mean almost anything.

Some focus mostly on investments. Some lead with insurance. Some work mainly with young families or business owners. If you are retired or close to it, you want a retirement financial advisor in Spokane who can coordinate the big moving pieces at once:

- 401(k) rollover decisions

- Roth conversion planning

- Social Security timing

- Retirement income planning

- Tax-efficient withdrawal strategies

- Medicare and IRMAA planning

- Qualified charitable distributions

- Estate planning coordination

- Investment management during retirement

The risk with a generalist is not that they give bad advice. It is that they give technically correct advice in one area while missing how it ripples into the rest of your plan.

A Roth conversion can look smart on its own, then quietly raise your Medicare premiums. Claiming Social Security early can feel comfortable, then reduce lifetime income for a surviving spouse. Retirement is not one decision. It is a series of connected ones.

3. Do they provide tax-aware retirement planning?

For many Spokane retirees, taxes are the single biggest planning opportunity, and Washington makes that especially true.

Washington has no state income tax, which can make planning interesting for people with large pre-tax accounts. If most of your savings sit in a traditional 401(k) or IRA, nearly every future withdrawal is taxable at the federal level. Once required minimum distributions begin, you have far less control over your tax picture.

A strong retirement advisor should help you think through:

- Should I do Roth conversions before RMDs begin?

- How do I sequence withdrawals across taxable, tax-deferred, and Roth accounts?

- Will my income push me into higher Medicare IRMAA premiums?

- How will my Social Security be taxed?

- Should I use qualified charitable distributions once I am eligible?

- How do I coordinate all of this with my CPA?

We do not replace your CPA, and we do not prepare your return. What we do is help coordinate retirement decisions with taxes in mind.

That distinction is the whole point. A tax preparer usually looks backward and reports what already happened. A tax-aware advisor looks forward and asks, "What should we do before December 31st to make this plan more efficient?" The window between retirement and RMDs is often where that planning pays off most.

4. Do they understand the decisions a large account creates?

Many people start looking for a financial advisor in Spokane because they want help with investments. That is reasonable. But for retirees, investments are only one piece.

If you have $1 million or more in a 401(k), the harder questions are usually:

- How do I turn this into reliable monthly income?

- How much can I safely spend?

- Should I move money to a Roth IRA, and how much?

- Should I delay Social Security?

- How do I give to charity in the most tax-efficient way?

These overlap constantly. Picture a Spokane retiree with a large traditional IRA who gives regularly to their church and is weighing Roth conversions. The right answer depends on their bracket, age, giving plans, Social Security timing, Medicare premiums, and estate goals all at once. A portfolio-only conversation will miss most of that.

When you interview an advisor, ask how they actually approach Roth conversion analysis, withdrawal sequencing, Social Security timing, and survivor planning for a spouse. If the conversation never leaves portfolio performance, that tells you something.

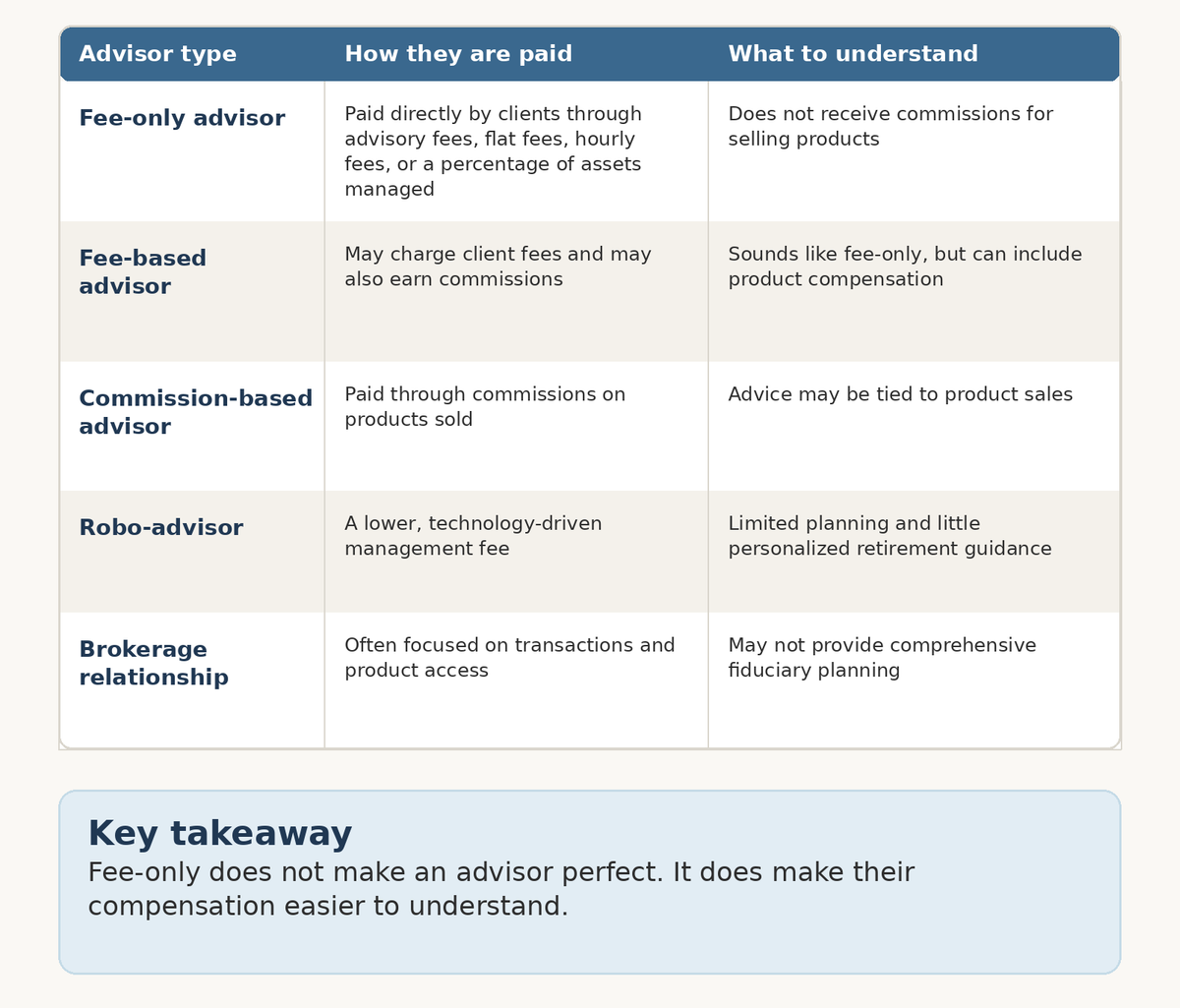

5. Are they fee-only, fee-based, or commission-based?

This may be the most important question you ask. The terms sound alike. They are not.

We are a fee-only fiduciary firm. We are paid by our clients, not by commissions from selling insurance, annuities, mutual funds, or other products. When you are deciding what to do with a large 401(k), or whether to buy an annuity, knowing exactly how the person advising you gets paid is not a small detail.

Before you hire anyone, ask whether they earn commissions, sell annuities or insurance, or have referral or revenue-sharing arrangements, and whether they will put every cost in writing. If the answer is hard to follow, pay attention to that.

6. Are they a fiduciary at all times?

A fiduciary is required to act in your best interest. Most people assume every advisor does that all the time. The industry is more complicated than that.

Some advisors act as a fiduciary in certain situations but not others. Some work for firms built around selling products. Some use titles that sound like planning but are still tied to sales.

So ask plainly: Are you a fiduciary at all times, and will you put that in writing? Are you acting as a fiduciary when you recommend a rollover, or when you discuss annuities? What conflicts of interest should I know about?

You can also do your own homework. Look up a firm through the SEC's Investment Adviser Public Disclosure site and read its Form ADV, which covers services, fees, conflicts, and disciplinary history. If an advisor holds the CFP designation, you can confirm it through CFP Board's verification tool. None of this replaces your own judgment, but these are easy checks worth making.

7. How do they manage investments for retirees?

Investing in retirement is a different job than investing while you work.

Before retirement, a downturn is uncomfortable, but you still have a paycheck, time to recover, and ongoing contributions. In retirement, you may be withdrawing from the portfolio while the market is down, which is a different kind of risk entirely.

A retirement-focused investment strategy should account for how much income you need, how much to hold in cash and short-term reserves, how withdrawals will be funded, how taxes affect the decisions, and how to avoid emotional moves during a rough market.

The goal is not the flashiest portfolio. It is an investment strategy that quietly supports your life. For a Spokane retiree with a large 401(k), that means connecting the portfolio to the income plan. If you need $6,000 a month, the strategy should reflect that. If you are doing Roth conversions, the advisor should know where the tax money comes from. Investments should never be managed in isolation.

Red flags to watch for

Not every advisor is the right fit. A few warning signs:

They cannot clearly explain how they are paid. If the answer to a fee question is vague or dismissive, be careful.

They lead with products instead of planning. If the first conversation is about buying an annuity or moving your account, that is backward. The first step should be understanding your goals, income needs, and tax picture.

They recommend a rollover too quickly. A 401(k) rollover can make sense, but it should never be automatic. A good advisor weighs your current plan's options, fees, creditor protections, and Roth choices first.

They only talk about performance. If taxes, income, Social Security, Medicare, and estate coordination never come up, you are not getting full planning.

They pressure you to act fast. Urgency, scarcity, and fear are sales tactics. Retirement decisions deserve time, questions, and a conversation with your spouse.

They do not work with people in your stage of life. If you are nearing retirement with a substantial 401(k), you want someone who handles those decisions every week, not someone who mostly serves young accumulators.

What to ask in the first meeting

Before you hire a Spokane financial advisor, consider asking:

- Who do you primarily work with?

- How are you paid, and are you fee-only, fee-based, or commission-based?

- Are you a fiduciary at all times?

- How do you approach Roth conversions and Social Security timing?

- Do you help with tax-aware withdrawal planning?

- How do you coordinate with my CPA or estate attorney?

- Who will I actually work with, and how often will we meet?

- What are your minimums and fees?

- What would make someone not a good fit for your firm?

That last one matters. A good advisor can tell you honestly who they serve well and who they do not.

How often should you meet with your advisor?

The right rhythm depends on your situation. For most retirees, annual or semiannual meetings work well, with extra conversations when a big decision comes up: a rollover, a Roth conversion, the sale of a business or property, the loss of a spouse, or a change in health.

A good review should go well beyond your portfolio. It should touch your income plan, tax picture, allocation, beneficiary designations, charitable giving, and any decisions on the horizon.

How much do Spokane financial advisors usually charge?

Fees vary by model. Common structures include a percentage of assets under management, a flat planning fee, an hourly rate, a retainer, commissions, or some mix of fees and commissions.

We offer ongoing planning and investment management with an AUM fee that starts at 1% and a $3,000 annual minimum. Separately, we offer a one-time financial plan for a flat fee of $3,000.

The number matters, but the better question is what you receive for it. Good advice can cover investment management, tax-aware withdrawals, Roth conversions, Social Security timing, QCDs, and estate coordination, and it can help you avoid mistakes that cost far more than the fee. A lower fee is not always better if the advice is thin, and a higher fee is not automatically worth it either. What matters is the value, the scope, and the conflicts.

What should Spokane retirees look for specifically?

If you are searching for the best financial advisor in Spokane, the better question is: best for whom?

The best advisor for a young business owner is probably not the best advisor for a retired couple living off their savings. For Spokane retirees and pre-retirees with substantial accounts, look for someone who can help with retirement income, tax-aware withdrawals, Roth conversions, Social Security timing, QCDs, investment management, 401(k) rollover decisions, estate coordination, and long-term planning for a surviving spouse.

Local situations come up too. Someone retiring from Avista may have pension and 401(k) decisions to coordinate. Someone leaving Providence may have a 403(b), a pension, or other plan options to weigh. Someone who spent decades saving into a pre-tax account may need help deciding how much to convert to Roth before RMDs begin. These are retirement planning questions, not just investment ones.

Is Stewardship Concepts Financial Services a good fit?

We are a Spokane-based, fee-only fiduciary financial planning firm, and we have worked primarily with retirees and people nearing retirement for over 28 years.

We tend to be a good fit for people who:

- Are retired or within about five years of retirement

- Have saved diligently in a 401(k), IRA, or 403(b), often $1 million or more

- Want help with Roth conversions, Social Security, and retirement income

- Care about tax-aware planning

- Want investment management connected to an actual plan

- Prefer a fee-only fiduciary relationship and do not want to be sold insurance or commission products

- Want a local Spokane team they can sit down with and call when questions come up

We are not the right fit for everyone. our ongoing planning and investment management fee starts at 1% of assets under management with a $3,000 annual minimum. Separately, we offer a one-time financial plan for a flat fee of $3,000. Many of the households we serve have $1 million or more, but that is the profile we work with most, not a hard requirement. If you would rather begin with a one-time engagement, we also offer a standalone financial plan for a flat fee of $3,000.

The most important thing is finding an advisor who fits your situation, your values, and the complexity of the decisions in front of you.

Ready to talk with a Spokane retirement financial advisor?

If you are retired or nearing retirement and have built substantial savings in a 401(k), IRA, or 403(b), the advisor you choose will shape decisions that follow you for decades.

We help Spokane retirees and pre-retirees make confident decisions about retirement income, Roth conversions, Social Security, investments, charitable giving, and taxes, all under one fee-only fiduciary roof.

If that is the kind of partner you are looking for, we would be glad to start a conversation.

Schedule a discovery call here

FAQ Section

1. How do I choose a financial advisor in Spokane?

Start with an advisor who works with people in your stage of life. If you are retired or nearing retirement, look for someone who regularly helps with retirement income, 401(k) rollovers, Roth conversions, Social Security, tax-aware planning, and investment management. Then confirm how they are paid, whether they are a fiduciary at all times, and exactly what services are included.

2. Should I work with a fee-only financial advisor in Spokane?

A fee-only advisor is paid by clients rather than by commissions on products they sell, which makes the relationship more transparent and removes certain conflicts of interest. It is not the only thing to weigh, but for retirees who want advice that is not tied to a product sale, it is an important one.

3. What is the difference between fee-only and fee-based?

Fee-only advisors are paid only by clients. Fee-based advisors may charge client fees but can also earn commissions or other product-related compensation. The terms sound nearly identical, so always ask exactly how the advisor is paid and ask for it in writing.

4. How much does a financial advisor in Spokane cost?

It varies by model. Some charge a percentage of assets under management, others use flat fees, hourly rates, retainers, or commissions. At Stewardship Concepts Financial Services, our ongoing planning and investment management fee starts at 1% of assets under management with a $3,000 annual minimum, and we also offer standalone retirement planning for a flat fee.

5. What is a red flag when choosing a financial advisor?

Common red flags include unclear fees, product-first recommendations, pressure to act quickly, rollover advice given without analysis, vague answers about fiduciary duty, and little discussion of taxes, income planning, or Social Security.

6. Do I need a financial advisor if I have $1 million in a 401(k)?

Not everyone needs one, but a large 401(k) creates real decisions: how to invest it, whether to roll it over, how to create income, whether and how much to convert to Roth, how withdrawals are taxed, when to claim Social Security, and how to coordinate giving and estate planning. A good advisor helps you organize those choices instead of facing them one at a time.

7. Should my financial advisor help with taxes?

Your advisor does not need to replace your CPA, but they should understand how taxes shape retirement decisions. For retirees that often means Roth conversions, withdrawal sequencing, QCDs, Social Security taxation, Medicare IRMAA planning, and capital gains timing, all coordinated with your tax preparer.

8. How often should I meet with my financial advisor?

Many retirees do well meeting once or twice a year, with extra meetings when a major decision comes up. The more complex your situation, the more valuable ongoing planning conversations become, rather than just an annual investment review.

About the Author

Noah Schwab, CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax, and financial planning

Noah Schwab, CFP®, is a Spokane financial advisor specializing in helping retirees with tax-efficient retirement income strategies, Roth conversions, and estate planning. This article is for educational purposes only and should not be considered tax or legal advice.