Roth Conversion Planning for Retirees and Near-Retirees

We help you think through whether Roth conversions may fit your retirement income, tax, Social Security, and long-term planning goals.

A Roth conversion can be helpful in the right situation, but it should be evaluated carefully before you move forward.

Fee-only fiduciary | CFP® professionals | 50+ years combined experience | Spokane-based

Who this is for

You may be in the right place if…

Roth conversions become more important to evaluate when retirement is getting close and most of your savings are in tax-deferred accounts.

You have a large 401(k) or IRA

You have meaningful savings in tax-deferred accounts and want to understand how future withdrawals, RMDs, and taxes may affect your retirement plan.

You are nearing retirement or already retired

You may have a window of time where Roth conversions could be worth evaluating before future income, Social Security, or required distributions change your tax picture.

You want to avoid costly tax surprises

You want help thinking through how Roth conversions may affect taxes, Medicare premiums, Social Security, retirement income, and long-term goals.

That’s where thoughtful Roth conversion planning can help.

What we help you decide

What Roth Conversion Planning Helps You Decide

A Roth conversion is not just a tax move. It is a retirement planning decision that should fit your income needs, tax picture, and long-term goals.

Whether a Roth conversion makes sense

We help evaluate whether converting part of a 401(k) or IRA to a Roth account may fit your broader retirement plan.

How much to convert

The right amount depends on your income, tax bracket, Medicare situation, cash flow, and long-term goals.

When to convert

Timing matters. We help you think through whether certain years may be more favorable based on retirement income, Social Security, and future required distributions.

How to pay the taxes

A conversion usually creates taxable income. We help you think through how the tax bill may be paid and whether the tradeoff makes sense.

How Medicare and Social Security may be affected

A Roth conversion can increase taxable income, which may affect Medicare premiums or Social Security taxation. These impacts should be considered before converting.

How Roth assets fit your long-term plan

Roth accounts may create future tax flexibility and can be part of a broader retirement income or legacy planning strategy.

The goal is not to convert just because you can. The goal is to decide whether a conversion fits your life, taxes, and retirement plan.

Why it matters

Why Roth Conversions Can Matter in Retirement

Many retirees enter retirement with most of their savings in tax-deferred accounts like 401(k)s and traditional IRAs. That can create important tax decisions later, especially when withdrawals, required minimum distributions, Social Security, investment income, and Medicare premiums begin to overlap.

A Roth conversion may help create more tax flexibility in the future, but it can also increase taxes today. That is why the decision should be made carefully, with a clear understanding of your income, tax bracket, Medicare situation, withdrawal strategy, and long-term goals.

For many retirees, the real question is not simply, “Should I convert?” It is, “How does this decision fit into the rest of my retirement plan?”

How we help

How We Help With Roth Conversion Planning

We help retirees and near-retirees evaluate Roth conversions as part of a larger retirement plan, not as a one-size-fits-all tax tactic.

Review your retirement income picture

We look at how your income may change over time, including withdrawals, Social Security, pensions, investment income, and other retirement resources.

Evaluate your tax situation

We review how a conversion may affect your taxable income today and how it could influence future tax planning opportunities.

Consider timing and conversion amounts

We help think through whether a conversion may make sense now, later, or not at all, and how much may be appropriate to evaluate.

Coordinate with your broader retirement plan

Roth conversion planning should work alongside your investment strategy, withdrawal plan, Social Security timing, and long-term goals.

Identify potential tradeoffs

A conversion can create benefits and drawbacks. We help you understand the tradeoffs before making a decision.

Work with your tax professional

We coordinate with your CPA or tax professional when appropriate so Roth conversion decisions fit your overall tax picture.

Important tradeoffs

When a Roth Conversion May or May Not Make Sense

Roth conversions can be valuable in the right situation, but they are not right for everyone.

A Roth conversion may be worth evaluating if…

- You expect your tax rate may be higher later

- You have large balances in a 401(k) or traditional IRA

- You are retired but not yet taking required minimum distributions

- You want more flexibility in future retirement income planning

- You want to reduce future tax pressure from tax-deferred accounts

- You are thinking about legacy planning for heirs

A Roth conversion may not make sense if…

- The tax cost today is too high

- It could push you into an unfavorable tax situation

- It may significantly increase Medicare premiums

- You need the money soon and do not have enough time for the strategy to work

- You do not have cash available to pay the tax bill

- The conversion does not fit your broader financial plan

The right answer depends on your situation. That is why Roth conversion planning should be personalized.

Why us

Why Retirees Choose Stewardship Concepts

You are not just deciding whether to move money from one account to another. You are making a tax-sensitive retirement decision that should fit your bigger plan.

A tax-smart approach to retirement

We help you think through Roth conversions, retirement income, future withdrawals, and other tax-sensitive decisions with an eye toward what you keep after taxes.

Fee-only fiduciary advice

Our guidance is built around your best interest, without commissions or product sales getting in the way.

A Spokane team that understands retirement planning

You work with a local team that understands the questions people face as retirement gets closer and financial decisions become more interconnected.

The process

What the First Conversation Looks Like

Starting the conversation does not mean committing to anything. It is simply a chance to talk through your situation, ask questions, and see whether we are a good fit.

Step 1: Schedule a Discovery Call

We’ll talk about where you are now, what questions are on your mind, and whether Roth conversion planning may be relevant to your situation.

Step 2: Review What Matters Most

If it looks like a fit, we’ll review the key parts of your retirement, tax, and income picture so we can better understand your planning opportunities.

Step 3: Choose the Right Next Step

Whether that means a standalone retirement plan, ongoing advice, or simply helping you think through your options, our goal is to help you move forward with clarity.

Not ready to meet?

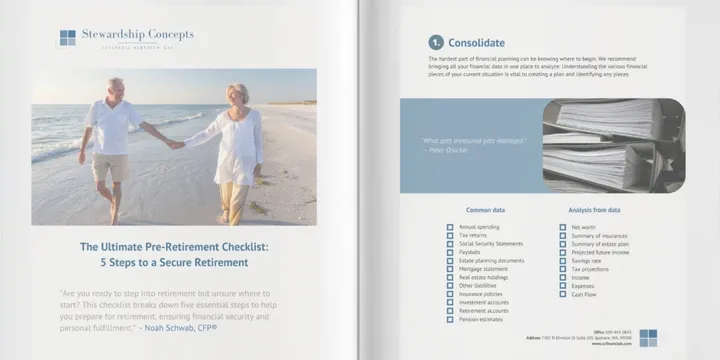

Download the Free Roth Conversion Guide

If you are still learning whether a Roth conversion may make sense, start with our free guide: Should You Do a Roth Conversion?

This guide walks through 10 questions to consider before making a Roth conversion decision.

- When Roth conversions may make sense

- How conversions can affect taxes, Medicare, and Social Security

- Common mistakes to avoid before converting

- How Roth conversions can fit into a larger retirement plan

Questions

Roth Conversion Planning FAQ

-

What is a Roth conversion?

A Roth conversion is when money is moved from a tax-deferred account, such as a traditional IRA or 401(k), into a Roth account. The converted amount is generally taxable in the year of conversion, but future qualified Roth withdrawals may be tax-free.

-

Are Roth conversions right for everyone?

No. Roth conversions can be helpful in some situations, but they are not right for everyone. A conversion may increase your taxable income in the year it is completed, so it should be evaluated carefully.

-

When should I consider a Roth conversion?

Roth conversions are often worth evaluating when retirement is approaching, income is changing, or there may be a window before required minimum distributions begin. The right timing depends on your tax situation, income needs, Medicare considerations, and long-term goals.

-

How do Roth conversions affect Medicare premiums?

A Roth conversion can increase taxable income, which may affect Medicare IRMAA premiums in a future year. That does not automatically mean a conversion is a bad idea, but Medicare impact should be part of the analysis.

-

Can I convert money from a 401(k) to a Roth IRA?

In many cases, retirees can evaluate converting tax-deferred retirement assets to a Roth IRA after rolling a 401(k) into an IRA, but the details depend on your plan rules, tax situation, and overall goals. This should be reviewed before taking action.

-

How much should I convert?

There is no one-size-fits-all answer. The right amount depends on your income, tax bracket, future withdrawal needs, Medicare situation, estate goals, and the rest of your retirement plan.

-

Do you prepare tax returns?

No. We do not prepare tax returns. We help with tax-aware retirement planning and can coordinate with your CPA or tax professional when appropriate.

-

Can you help me decide whether a Roth conversion fits my retirement plan?

Yes. We help retirees and near-retirees evaluate Roth conversions as part of a broader retirement income, tax, and investment strategy.

Take the next step

Let’s See Whether We’re a Fit

If you are nearing retirement or already retired and want help deciding whether Roth conversions fit your retirement plan, start with a discovery call.

We work best with retirees and near-retirees who want thoughtful guidance on retirement income, taxes, large 401(k)s, Roth conversions, and the bigger financial decisions ahead.

Fee-only fiduciary advice · Spokane-based · CFP® professionals

Questions before scheduling? We would be glad to help.

509-443-0845 Kate@scfinancials.com Spokane, Washington

Roth conversion strategies may not be appropriate for all investors. The potential benefits of a Roth conversion depend on individual circumstances, tax law, timing, and future market conditions.