For high-income earners, contributing directly to a Roth IRA isn’t always possible because of IRS income limits. In 2025, eligibility phases out completely at $161,999 for singles and $240,000 for married couples filing jointly.

The Backdoor Roth IRA is a legal strategy that allows you to sidestep these limits and still benefit from Roth growth and withdrawals. In this guide, we’ll break down how the strategy works, common pitfalls, the 5-year rules, and planning tips to make the most of it.

What Is a Backdoor Roth IRA?

A Backdoor Roth IRA is not a special type of account—it’s a strategy:

- Make a non-deductible contribution to a Traditional IRA.

- Convert those funds to a Roth IRA.

- Report the transaction correctly on your tax return.

The converted funds then grow tax-free, and in retirement, qualified withdrawals are also tax-free.

Step-by-Step: How a Backdoor Roth Works

- Open a Traditional IRA

- Contribution limit in 2025: $7,000 ($8,000 if age 50+).

- Contribution must be from earned income (wages, salary, self-employment income).

- If you don’t have earned income, you may use a spousal IRA if your spouse does.

- Convert to a Roth IRA

- After your contribution posts, convert it to a Roth IRA.

- Many people convert quickly to avoid taxable gains.

- Report on Taxes

- Use IRS Form 8606 to document the non-deductible contribution and the Roth conversion.

- This ensures you don’t get taxed twice.

The Pro-Rata Rule: Why Existing IRA Balances Matter

The IRS requires you to calculate Roth conversion taxes across all your IRAs (Traditional, SEP, SIMPLE), not just the account you’re converting.

- Example: If 80% of your IRA balances are pre-tax, then 80% of your conversion is taxable, even if you were only trying to move after-tax money.

- This makes a Backdoor Roth “clean” only if you don’t have other pre-tax IRA balances.

Tip: You can often roll pre-tax IRA funds into a 401(k) with your employer to avoid pro-rata complications.

The 5-Year Rule(s)

The term “5-year rule” is confusing because there are actually two different rules—one for earnings and one for conversions.

Order of Withdrawals (Important Foundation)

When you take money out of a Roth IRA, the IRS assumes it comes out in this order:

- Contributions (always tax and penalty-free)

- Conversions (oldest first, then taxable before non-taxable)

- Earnings (subject to the 5-year rule + age requirement)

The 5-Year Rule for Earnings

- To withdraw earnings tax and penalty-free, you must:

- Be age 59½ or older, AND

- Have had a Roth IRA open for at least 5 years.

- This 5-year clock starts with your first-ever Roth contribution.

The 5-Year Rule for Conversions (Backdoor Roths)

- Each conversion has its own 5-year clock.

- If you’re under 59½, withdrawing converted amounts within 5 years may trigger a 10% penalty.

- After age 59½, this rule no longer applies for penalty purposes, but the earnings 5-year rule still applies.

Benefits of a Backdoor Roth IRA

- Tax-Free Growth: Investments compound without taxes.

- Tax-Free Withdrawals: Qualified withdrawals in retirement are tax-free.

- No RMDs: Unlike Traditional IRAs, Roth IRAs don’t require withdrawals during your lifetime.

- Estate Planning Advantage: Beneficiaries inherit Roth IRAs income tax-free.

Common Mistakes to Avoid

- Ignoring the Pro-Rata Rule: Can lead to large, unexpected tax bills.

- Not Filing Form 8606: Required to avoid double taxation.

- Delaying Conversion: Investment gains between contribution and conversion are taxable.

- Over-Contributing: Contributions above the limit face a 6% annual penalty.

Tips for a Smooth Backdoor Roth

- Consult a CPA or CFP® before executing.

- Roll pre-tax IRA balances into an employer 401(k) if possible.

- Convert soon after contributing.

- Keep detailed records of contributions, conversions, and tax forms.

Who Should Consider a Backdoor Roth?

- High-income earners above Roth income limits.

- People without significant pre-tax IRA balances.

- Savers focused on long-term tax-free growth.

- Individuals incorporating Roth accounts into estate planning.

Strategic Timing

- Convert quickly: Don’t invest funds in the Traditional IRA before converting.

- Low-income years: Ideal for Roth conversions (e.g., during job change, retirement transition).

- 2025–2028 window: Current tax rates are historically low; consider acting before potential increases.

- Avoid December rush: Complete earlier in the year to reduce reporting errors.

Advanced Planning Integration

- Mega Backdoor Roth: Some 401(k)s allow large after-tax contributions and Roth rollovers.

- Roth Conversions: Pair partial IRA or 401(k) conversions with Backdoor Roths for tax optimization.

- Estate Planning: Combine Roth IRAs with other accounts for a tax-efficient legacy plan.

Behavioral Planning & Tax Projections

- Annual tax projections help determine how much to convert without jumping tax brackets (software like Holistaplan can help).

- Avoid procrastination: Market timing fears often cause delays—consistency is key.

- Coordinate with other tax strategies (charitable giving, deductions).

- Track everything: Keep accurate records for compliance and simplicity.

Case Studies

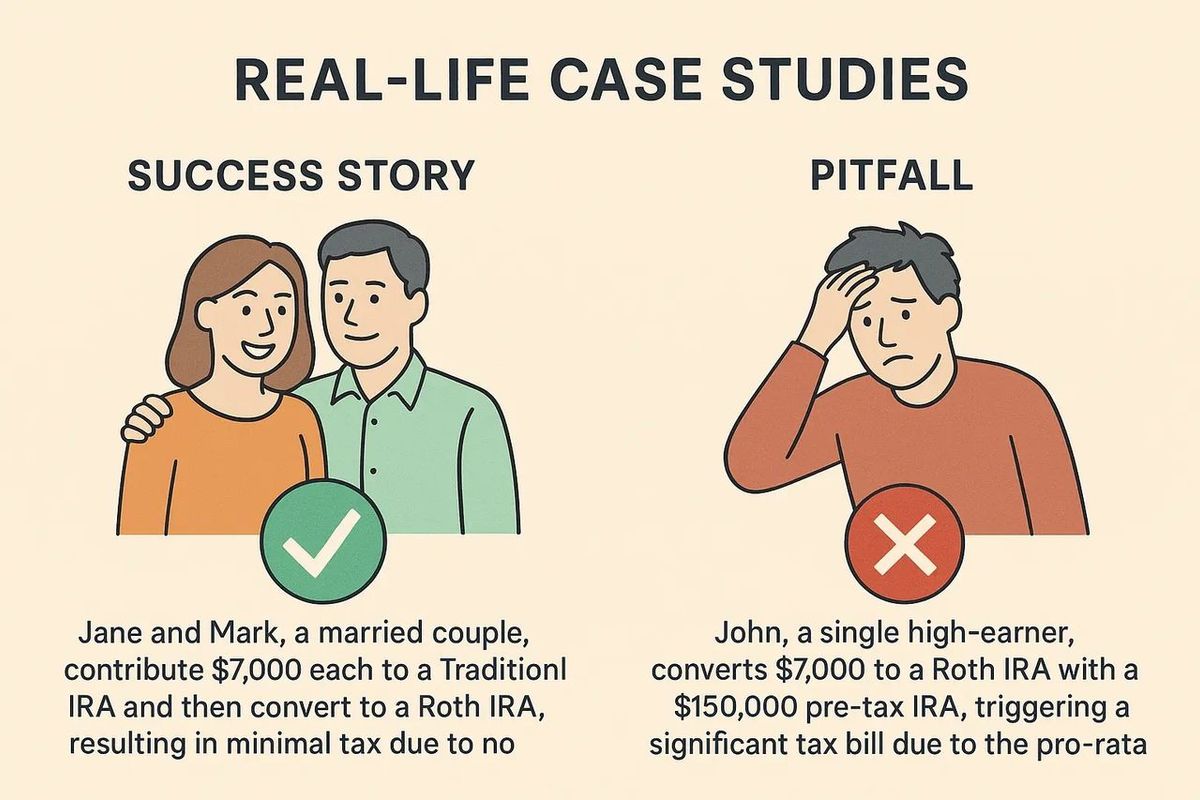

Success Story:

Jane and Mark (married, $300k income) maxed out 401(k)s and contributed $7,000 each to Traditional IRAs in January 2025. They converted to Roth the same week, had no other pre-tax IRA balances, and their conversion was tax-free. Their Roths now grow tax-free for life.

Pitfall:

John (single, high earner) had $150,000 in a pre-tax Traditional IRA. He converted a $7,000 contribution without considering the pro-rata rule. Result: 95% of his conversion was taxable, leading to a $6,650 tax bill.

FAQs

Q: What are the Roth IRA income limits in 2025?

A: Phaseout begins at $150,000 (single) / $236,000 (married) and ends at $161,999 (single) / $240,000 (married).

Q: Can I do a Backdoor Roth if I have a Traditional, SEP, or SIMPLE IRA?

A: Yes, but the pro-rata rule will likely make it less favorable.

Q: Do I pay taxes on the conversion?

A: If your contribution was non-deductible and you have no other pre-tax IRA balances, the conversion is usually tax-free. Otherwise, taxes may apply.

Q: What is the 5-year rule?

A: There are two rules: one for Roth earnings (applies to all Roths) and one for conversions (each has its own 5-year clock).

Q: What happens if I over-contribute?

A: Excess contributions face a 6% penalty each year until corrected.

Q: Do I need professional help?

A: Highly recommended to avoid mistakes and penalties.

Will the Backdoor Roth Last Forever?

Congress has debated shutting down the Backdoor Roth. While it’s currently legal, the IRS has never issued formal guidance on whether it violates the step-transaction rule (treating multiple steps as one). This adds some risk, so consult a professional before proceeding.

Final Thoughts

The Backdoor Roth IRA is a powerful, legal strategy for high-income earners who want tax-free retirement growth. Success depends on careful planning, accurate reporting, and awareness of the rules. With the right approach, you can lock in decades of tax-free compounding and create a more flexible retirement strategy.

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax and financial planning