A popular question that I get as a financial advisor is whether to recommend contributing money to a Roth IRA or a traditional IRA. There are positives and negatives to each. To be transparent, I can’t recommend one or the other without knowing someone’s individual circumstances. But I can talk about the similarities and differences between both and recommend you reach out to your financial advisor or CPA.

Similarities:

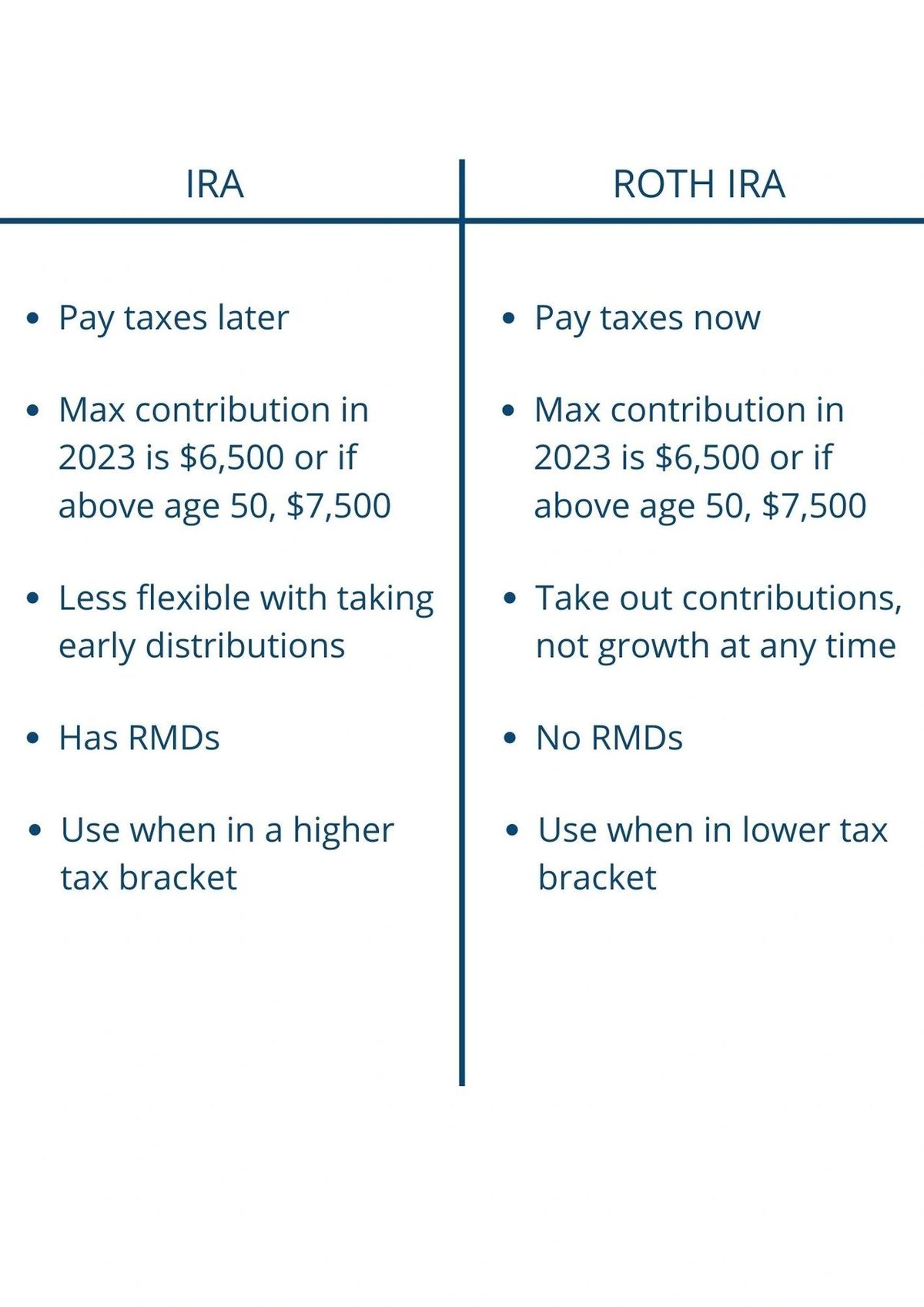

- Both offer tax benefits to help save for retirement and have the same maximum contribution amounts ($6,500 in 2023 or $7,500 if you are age 50 or older).

- Both can hold the same types of investments: stocks, bonds, ETFs, and mutual funds.

Differences:

- There are critical differences between Roth IRAs and traditional IRAs that determine which to use.

Contributions:

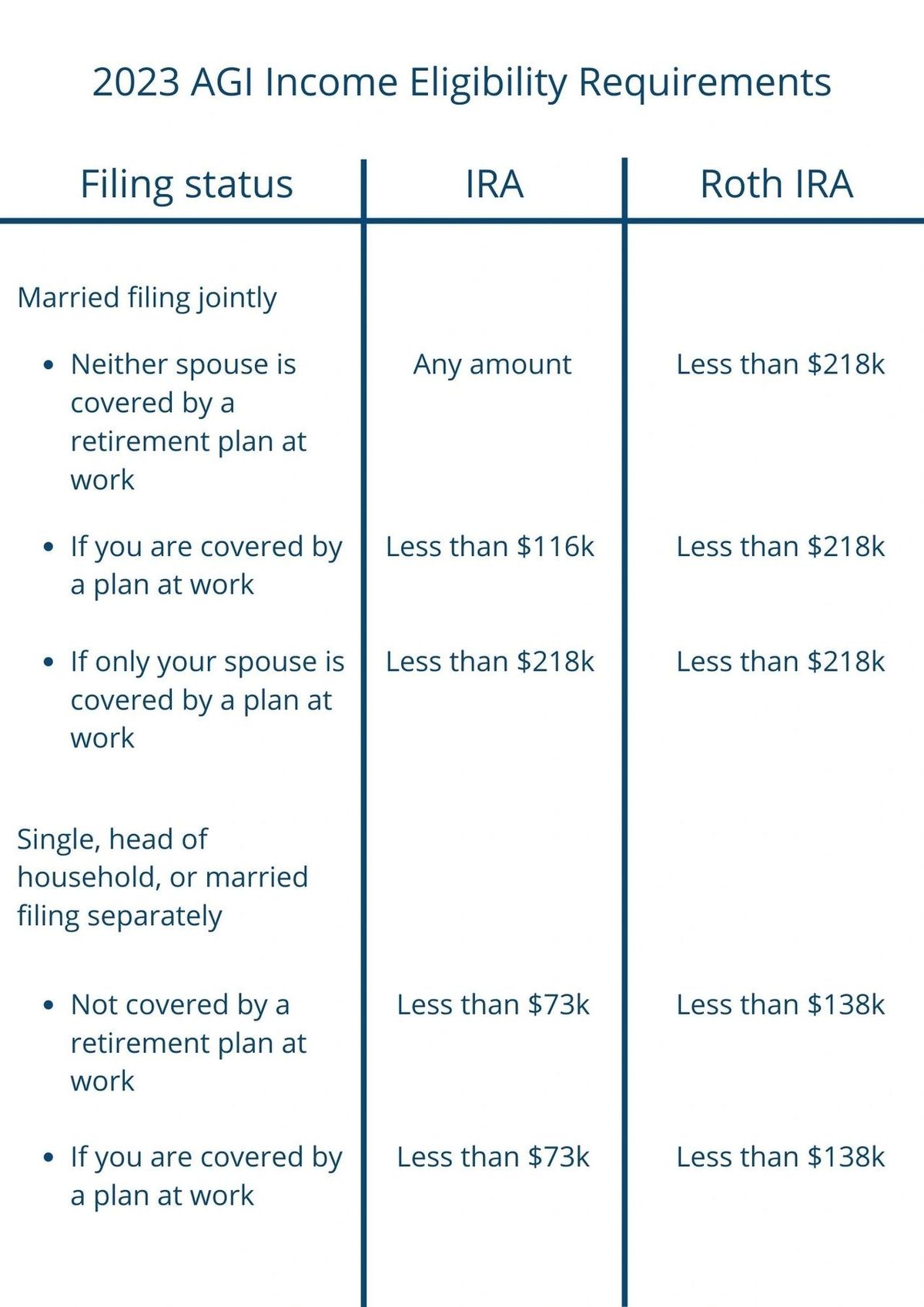

- With a traditional IRA, you will be able to reduce your taxable income by the amount that you contribute to a traditional IRA. You must follow requirements to be eligible, dependent on how much income you have for the year and whether you or your spouse is covered by a retirement plan that year.

- With a Roth IRA, contributions are made on an after-tax basis, so you cannot claim a tax deduction for them. However, there are less strict requirements to contribute to a Roth IRA for income and if you are covered by a retirement plan at work.

Taxes:

- With a traditional IRA, your contributions are tax-deductible within the guidelines. The growth and earnings are tax-deferred. You only pay taxes on the money that’s withdrawn in retirement. The benefit of this account is to pay fewer taxes because you’ll be in a lower tax bracket in retirement.

- With a Roth IRA, you pay taxes on the money you contribute up front, but your withdrawals in retirement are tax-free. Tax-free growth means you don’t pay taxes on any capital gains, dividends, or interest earned within the account.

Eligibility:

- Traditional IRAs do not have income limits, but you may not be able to claim a tax deduction on your contributions if you are covered by a retirement plan at work and your income exceeds certain limits.

- Roth IRAs have income limits even if you’re covered by a retirement plan at work, so you may not be eligible to contribute if your income is too high.

Withdrawal: Both traditional IRAs and Roth IRAs have rules governing when and how you can withdraw money from your account.

- With a traditional IRA, you must start taking required minimum distributions (RMDs) when you reach age 72.

- With a Roth IRA, you have greater flexibility because you can always take out your contributions at any time. But generally, you must wait until age 59.5 to avoid a 10% penalty.

- For both accounts, there are some exceptions to this rule like a $10,000 allowance for a first-time home purchase. Check here for additional exemptions to the penalty.

More information about Roth IRAs

- There are no required minimum distributions (RMDs): With a traditional IRA, you must start taking required minimum distributions (RMDs) at age 72 (70 1/2 if you reached age 70 1/2 before January 1, 2020). With a Roth IRA, there are no RMDs, which means you can leave your money in the account to grow tax-free for as long as you want.

- If you think that you’ll be in a higher tax bracket in retirement because of your income or because of future tax bracket increases, you’ll be money ahead in retirement for using a Roth IRA now.

More information about traditional IRAs

- Tax-deferred growth: The money in your traditional IRA grows tax-deferred, meaning you don't have to pay taxes on the investment income until you withdraw the money in retirement. This allows your savings to potentially grow faster than they would in a taxable investment account.

- Flexibility: You can contribute to a traditional IRA at any time and change your contribution amount from year to year as your financial situation changes.

- Required minimum distributions (RMDs): Traditional IRAs have a required minimum distribution (RMD) age of 72. This means that you must begin taking distributions from your traditional IRA when you reach the age of 72. The RMD rules do not apply to Roth IRAs.

- It's important to note that there are also income limits and contribution limits for traditional IRAs, and you may not be able to make a tax-deductible contribution if you or your spouse are covered by a retirement plan at work and your income is above a certain level. It's a good idea to consult with a financial professional or refer to IRS guidelines to determine whether a traditional IRA is right for you and how much you can contribute.

Rule of thumb

- To decide between Roth or traditional IRA contributions, you must compare your current and retirement tax bracket. If you are in a lower tax bracket now than you would be in retirement, Roth IRA contributions offer the most tax savings. If you’ll be in a lower tax bracket in retirement, it’s better to contribute to an IRA. Tax savings aren’t the only aspect to consider.

- Having a Roth IRA and a traditional IRA in retirement gives you more tools to reduce tax liability. For example, if you are purchasing a new car and had to withdraw all the amount from a traditional IRA, it could put you into a higher tax bracket. Alternatively, if you had both accounts you could withdraw from each and stay in the lower tax bracket.

Remember

When deciding between both accounts it’s important to check your income. The amount you can and should contribute will be limited based on your individual circumstance, and tax filing status. Check with a Spokane financial advisor or CPA to determine if an IRA or Roth IRA is the right choice for you based on your situation.

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington who specializes in helping Spokane small business owners.

- Synergizing business and personal finances

- Setting up retirement plans

- Investment management

Resources:

IRA and Roth IRA contribution rules: Link

Exemptions to the 10% penalty: Link

RMDs: Link