As a financial advisor in Spokane, I come across people who have made excellent efforts to save for retirement in their 401(k) or some other tax-deferred account. Unfortunately, many of them are unaware that there exists a highly effective tax strategy that can conserve thousands of dollars over the years. This strategy employs a period that we call the Retirement Valley.

What is the Retirement Valley?

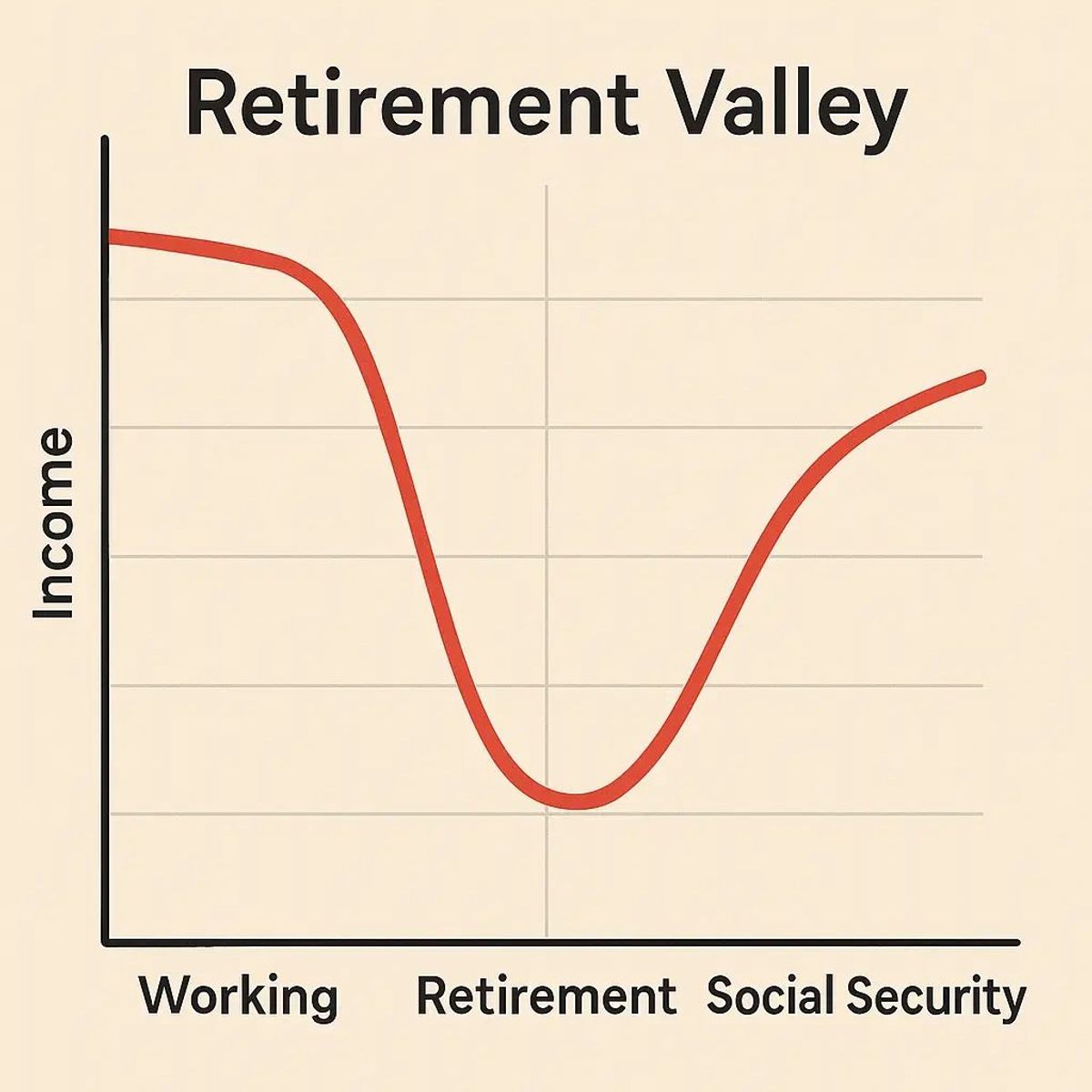

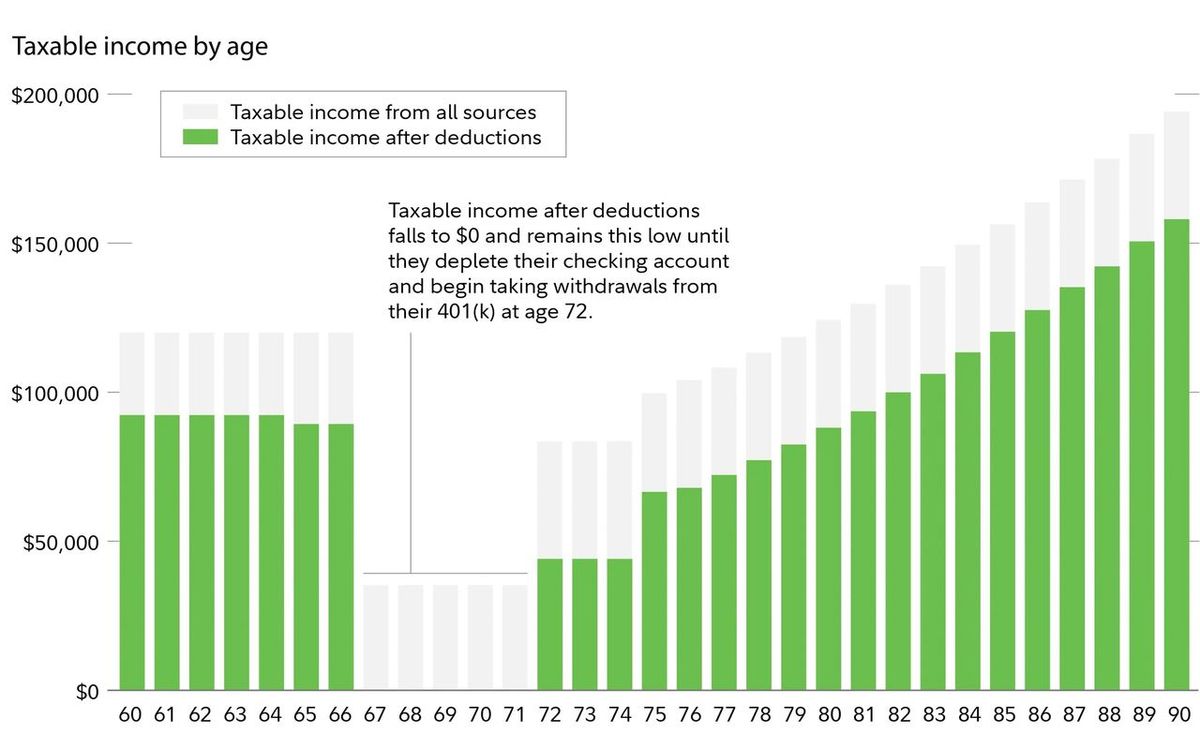

The Retirement Valley is the gap between the year you retire and the year that Social Security benefits or Required Minimum Distributions (RMDs) begin. It's a time that can be years or even a decade, where your taxable income can be much less than when you were employed.

By utilizing this window of lower tax rates, you have the opportunity to do more in terms of larger Roth conversions when you're paying less tax.

Why Build a Cash Cushion Pre-Retirement?

The most effective way to build flexibility during retirement is to build a cash cushion or a taxable investment account pre-retirement. This approach allows you to:

- Take money out of those accounts earlier in retirement

- Delay withdrawals from your 401(k) or IRA

- Delay claiming Social Security benefits, which will increase your lifetime benefits

- By doing so, you retain control over your taxable income in the first years of retirement and set yourself up to maximize the Retirement Valley.

How Roth Conversions in the Retirement Valley Work

A Roth conversion transfers funds from a regular 401(k) or IRA to a Roth IRA. The converted amount is taxable in the year of the conversion, but after that money is in the Roth IRA it accumulates tax-free for the remainder of your life. Converting these funds while in a lower tax bracket can save a tremendous amount of tax cost.

The advantages are:

- Lower future RMDs, which can help to keep your tax rate lower later on in retirement

- Less likelihood of paying higher Medicare premiums due to Income-Related Monthly Adjustment Amounts (IRMAA)

- Transferring tax-free Roth funds to heirs instead of taxable retirement accounts

Why Spokane Retirees Should Consider This Approach

The majority of Spokane retirees have saved the majority of their fortunes in pre-tax retirement funds. Without careful planning, these funds can cause surprisingly high taxes in retirement. As a Spokane financial planner, I've seen how optimizing the Retirement Valley for Roth conversions can significantly minimize a retiree's lifetime tax burden.

Even if you are a couple of years away from retiring, it's the ideal time to start building that cash cushion and creating a withdrawal strategy that aligns with your tax planning goals.

Take the Next Step

If you are nearing retirement and would like to discuss how the Retirement Valley might be of value to you, I can assist you in calculating the numbers and determining how it would be a good fit within your overall plan. Each person's circumstances are different and timing is everything for this strategy to be effective.

To talk with a Spokane financial advisor who understands how to put together Roth conversions, Social Security timing, and tax-deferred withdrawal strategies schedule a no-cost, no-commitment discovery call today.

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax and financial planning