Financial Planning: IRMAA 101 — What Every Retiree Should Know

For many retirees, Medicare feels like a welcome relief after decades of paying for private health insurance. But there’s one part of Medicare that often catches retirees off guard: IRMAA, the Income-Related Monthly Adjustment Amount.

As a financial advisor in Spokane, I see IRMAA surprise retirees more than almost any other retirement expense, especially those with high savings in 401(k)s, IRAs, or taxable investment accounts. And with Medicare premiums rising and tax brackets shifting due to legislation like the SECURE Act and the One Big Beautiful Bill Act, planning for IRMAA has never been more critical.

This article breaks down the essentials of IRMAA, how it’s calculated, how it affects your retirement plan, and strategies to minimize it, particularly if you're doing Roth conversions, taking RMDs, selling investments, business, or home, or navigating a transition into retirement.

What Is IRMAA?

IRMAA is an additional surcharge added to Medicare Part B (outpatient services) and Part D (prescription plans) for retirees with higher incomes.

Medicare uses a tiered income system. If your modified adjusted gross income (MAGI) surpasses certain thresholds, you’re bumped into an IRMAA bracket and pay higher monthly premiums for the entire year.

Why IRMAA Matters

Most retirees budget based on standard Medicare premiums, only to discover later that their premiums are hundreds of dollars higher per month. That’s because:

- IRMAA applies automatically when income exceeds the threshold.

- It applies each calendar year, based on your tax return.

- Many retirees unintentionally trigger it through tax-efficient but income-raising strategies like Roth conversions.

For retirees on a fixed income, a surprise bill of $1,000–$6,000 per year in extra premiums can disrupt cash flow planning.

How Medicare Determines Whether You Owe IRMAA

Here’s the part that surprises almost everyone: Medicare uses your tax return from two years prior. So your 2025 Medicare premiums are based on your 2023 tax return. That means the financial decisions you make today, Roth conversions, realizing capital gains, and taking distributions, will affect your Medicare costs two years from now. This is why retirees working with a financial advisor in Spokane often build multi-year tax and income plans around IRMAA thresholds.

MAGI: The Number That Drives It All

IRMAA is calculated using your MAGI (Modified Adjusted Gross Income) and adding tax-exempt interest. For most retirees, MAGI is: Adjusted Gross Income (AGI) + tax-exempt interest

What Counts as Tax-Exempt Interest?

Tax-exempt interest includes:

- Interest from municipal bonds (state, city, county, or certain U.S. territories)

- Interest from municipal bond mutual funds or ETFs

- Zero-coupon municipal bonds (the imputed interest still counts)

- Interest from private activity bonds (this applies to fewer retirees)

Even though this interest is federally tax-free, Medicare still adds it back when calculating IRMAA.

What Makes Up Your AGI?

AGI includes income from sources such as:

- Roth conversions

- Required Minimum Distributions (RMDs)

- Capital gains (from selling investments, property, or a business)

- Dividends and interest

- Pension income

- Consulting or part-time work

- Traditional IRA and 401(k) withdrawals

- Annuity income

- The taxable portion of Social Security

You can usually find your AGI on line 11 of your personal tax return.

If you're still working, contributions to retirement plans, such as a 401(k), 403(b), or traditional IRA, can reduce your AGI. But keep in mind: even one-time income events, like selling a rental property, can push you into a higher IRMAA bracket for the next year. Here are the IRMAA brackets for 2025. Remember that these rates will adjust over time:

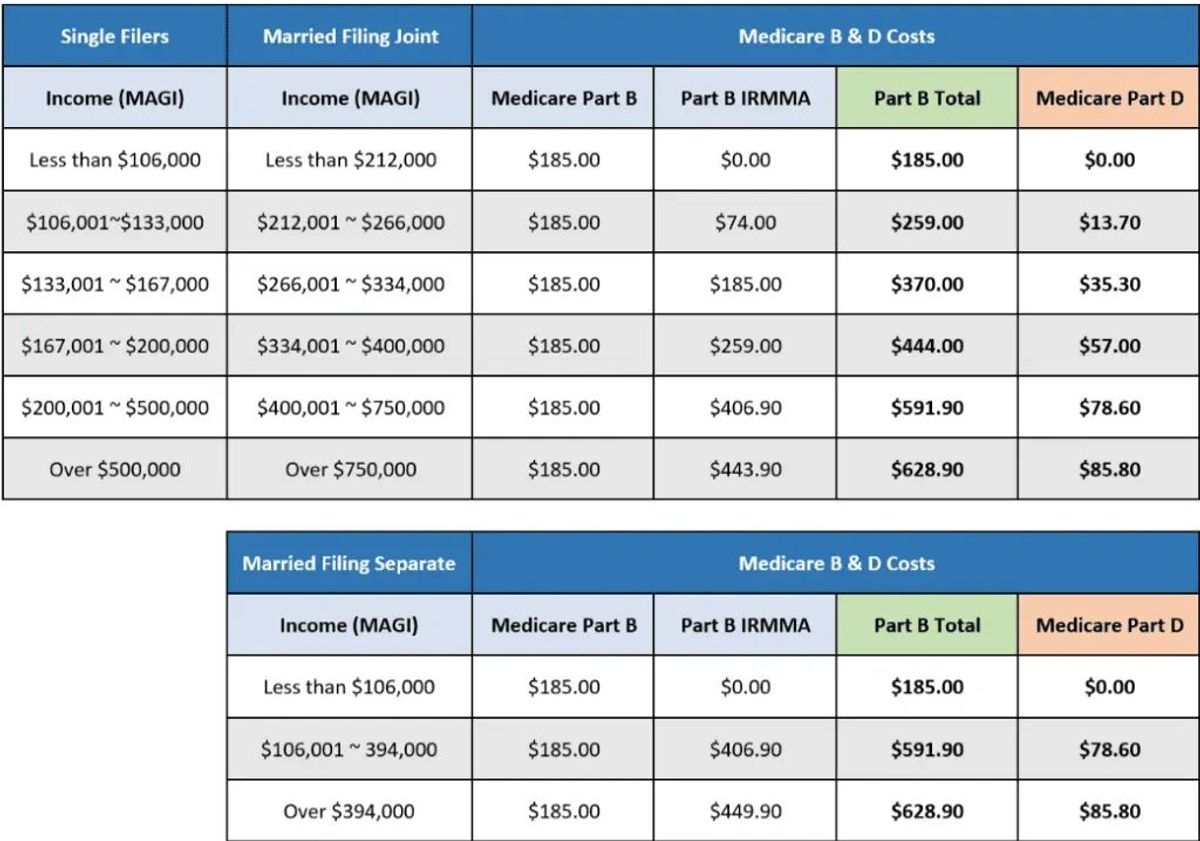

The IRMAA Brackets

IRMAA brackets adjust annually for inflation, but here’s the general structure:

- Standard Medicare premiums (no IRMAA if you’re below the threshold)

- Add IRMAA tiers, each increasing your Part B and Part D premiums

The jump from one tier to the next can be dramatic: $600 to $3,000+ per year per person. And because IRMAA is applied per person, a married couple can pay double if both are enrolled in Medicare.

Why IRMAA Planning Matters for Retirees

IRMAA isn’t just about Medicare premiums; it’s about managing total lifetime taxes. Retirees often make what appears to be a smart tax move, such as doing a large Roth conversion, only to later discover they triggered thousands in extra Medicare premiums. Common scenarios that unintentionally push retirees into IRMAA:

1. Roth Conversions

Roth conversions can be one of the best long-term tax strategies, especially for retirees with large 401(k) balances. But since conversions count as ordinary income, they can push MAGI well above IRMAA thresholds. Smart retirees convert up to the edge of a bracket, not through it.

2. High RMDs in Your 70s

Many retirees are shocked by how large their RMDs become once required distributions begin. RMDs often add $40,000–$100,000+ of annual income, which can trigger IRMAA every year.

3. Realizing Capital Gains

Selling long-held investments, a rental property, or a business interest can spike income. This often blindsides new retirees.

4. Strategic Timing of Social Security

Once you turn on Social Security, your MAGI typically jumps, reducing flexibility for Roth conversions and tax planning.

5. Timing Part-Time Work or Consulting

Even small amounts of income can push retirees across an IRMAA line.

This is where having a financial advisor in Spokane who specializes in multi-year tax planning makes a real difference. We use powerful planning software, like Holistiplan, to evaluate your tax picture, avoid surprises, and guide you toward the most effective strategy.

How IRMAA Affects Part B and Part D Premiums

Let’s break down how IRMAA impacts both premium types:

Medicare Part B (Medical Insurance)

The standard Part B premium applies for lower-income retirees. IRMAA adds a surcharge, often hundreds of dollars a month at higher brackets.

Medicare Part D (Prescription Drug Coverage)

Part D IRMAA is smaller but still meaningful, usually ranging from $12–$80 per month depending on the tier.

These amounts are recalculated each year.

How to Appeal IRMAA

Here’s the good news: if your income has gone down because of a qualifying life event, you can appeal IRMAA. This is especially helpful for retirees who receive IRMAA in their first year of retirement but no longer have high income. To appeal, you use Form SSA-44 and provide documentation of your income change. A financial advisor can help you complete the form correctly to avoid delays.

Common Qualifying Life Events

- Retirement

- Reduction in work hours

- Loss of a pension

- Divorce

- Death of a spouse

- Loss of property-producing income

Strategies to Reduce or Avoid IRMAA

IRMAA avoidance is not always the goal; sometimes it’s better to convert into Roths and accept the IRMAA. But well-designed planning can often minimize surprises.

Here are the top strategies retirees in Spokane can use:

1. Do Roth Conversions Before Starting Medicare

This is one of the biggest value-add strategies for retirees in their 50s and early 60s. For many retirees, ages 60–64 are golden years for Roth conversions.For many retirees, ages 60–64 are golden years for Roth conversions.

Doing conversions before age 65 allows you to:

- Reduce future RMDs

- Fill lower tax brackets

- Lower lifetime taxes

- Avoid IRMAA when premiums begin

2. “Fill the Bracket.” Do Conversions Only Up to an IRMAA Line

A CFP® can map out how much you can convert before hitting the next IRMAA threshold. This helps maximize tax strategy without triggering thousands in extra Medicare premiums.

3. Time Capital Gains Carefully

If you plan to sell investments or property, choosing the right year matters. For example:

- The year before Medicare begins

- A year in which you have an unusually low income

- A year where conversions are not planned

Remember to avoid stacking high-income events in the same tax year.

4. Delay Social Security

Delaying Social Security gives you more room for Roth conversions in your 60s without triggering IRMAA.

This is especially useful for retirees with:

- Large pre-tax balances

- Widow(er) planning needs

- Pension income

- High future RMDs

5. Coordinate RMD Strategy

Once RMDs begin at 73, you lose flexibility. Reducing RMDs through early Roth conversions is one of the best long-term IRMAA strategies.

6. Manage Withdrawals Intentionally

Pulling income from these sources can help control your MAGI:

- Roth accounts

- Cash reserves

- Low-gain assets

7. Use QCDs (Qualified Charitable Distributions) After Age 70½

QCDs count toward your RMD but do not count as income on your tax return. This is one of the most powerful strategies for charitably inclined retirees.

Why IRMAA Planning Matters for Spokane Retirees Specifically

Spokane and Washington State retirees often face unique circumstances:

- Washington has no state income tax, making federal tax planning even more important.

- Many retirees here have large 401(k) balances from long Boeing, tech, medical, or public-sector careers.

- Our region has a large number of Providence, Kaiser, Avista, and municipal retirees—many with pensions that raise MAGI.

- Washington's estate tax influences Roth conversion timing, which indirectly affects IRMAA.

Working with a financial advisor in Spokane who understands these dynamics ensures your IRMAA planning integrates with:

- Roth conversions

- RMD strategy

- Pension timing

- Washington estate tax planning

- Medicare timelines

Effective IRMAA planning is a multi-year tax-planning strategy, not a one-time decision.

When Does Paying IRMAA Actually Make Sense?

Sometimes, the best long-term move is to intentionally trigger IRMAA in exchange for lower lifetime taxes. Paying an extra $1,500 in IRMAA to reduce future RMDs and save $10,000–$50,000 in taxes over your lifetime is a smart tradeoff. This is why blanket IRMAA avoidance can be dangerous.

Instead, retirees should seek the optimal balance:

- Pay IRMAA when the long-term benefits outweigh the short-term cost

- Avoid IRMAA in years when it's unnecessary

- Smooth income across years to reduce bracket creep

Frequently Asked Questions

Q: What is the purpose of IRMAA?

A: To require higher-income retirees to pay more for Medicare Part B and D premiums.

Q: How can I avoid IRMAA?

A: Manage MAGI by controlling Roth conversions, capital gains, RMDs, and timing of income.

Q: Does Social Security count toward IRMAA?

A: Yes, up to 85% of Social Security is included in MAGI.

Q: Can you appeal IRMAA?

A: Yes. Use Form SSA-44 after a qualifying life event such as retirement, loss of income, or the death of a spouse.

Q: Is IRMAA based on gross or taxable income?

A It’s based on modified adjusted gross income (MAGI).

Final Thoughts: IRMAA Shouldn’t Be a Surprise

IRMAA is one of the most overlooked costs in retirement, but it doesn’t need to catch you off guard. With thoughtful tax planning, careful timing, and strategic income management, you can control IRMAA and keep your Medicare costs predictable.

As a financial advisor in Spokane specializing in tax-efficient retirement planning, I help retirees:

- Plan Roth conversions intelligently

- Avoid unnecessary IRMAA surcharges

- Optimize Social Security

- Manage RMDs

- Coordinate pension and investment income

If you’re nearing Medicare age or already paying IRMAA, now is the perfect time to build a strategic plan with one of our Spokane financial advisors.

Meet with our Spokane Financial Advisor today

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax and financial planning

Noah Schwab, CFP®, is a Spokane financial advisor specializing in helping retirees with tax-efficient retirement income strategies, Roth conversions, and estate planning. This article is for educational purposes only and should not be considered tax or legal advice.