A Spokane Financial Advisor’s Guide to Making the Right Choice

As a Spokane financial advisor and CFP® who spends every day helping retirees and pre-retirees make smarter tax decisions, one question surfaces more than almost any other:

“Should I contribute to a Roth or a traditional (pre-tax) retirement account?”

It’s a simple question on the surface, but it carries enormous long-term implications. The answer can influence your lifetime tax bill, your retirement income strategy, the size of your future Required Minimum Distributions (RMDs), and even what you leave behind to your children.

Most online articles offer surface-level explanations of the differences between Roth and traditional accounts. But if you’re retiring in Washington State, navigating 401(k)s at Providence or other major Spokane employers, or planning around Social Security timing and the potential Washington State estate tax, you need a deeper, more strategic framework.

This guide gives you exactly that, an expert-level breakdown, written specifically for retirees and near-retirees in Spokane, WA.

The Core Question: Will Your Tax Rate Be Higher Today or Later?

Every conversation about Roth vs. traditional contributions begins with one fundamental question:

Do you expect your tax rate to be higher now or in retirement?

That’s the decision point.

If taxes will be higher later → Roth contributions make sense.

You pay tax now at a lower rate. Your future withdrawals are tax-free.

If taxes will be lower later, → Traditional (pre-tax) contributions make sense.

You get a deduction today, lowering your taxable income. You pay (or your heirs) taxes later, ideally at a lower rate.

This basic logic is sound. But in real-life financial planning, very few people have a clear picture of their future tax bracket. And almost no one realizes how many opportunities exist to intentionally shape those tax brackets in retirement.

That’s where strategic planning and the value of working with a Spokane financial advisor who specializes in tax-efficient retirement strategies come in.

Why Most Spokane Retirees Benefit From Traditional Contributions During Working Years

For the majority of clients I work with, typically individuals or couples retiring with $1 million or more in their 401(k). The optimal strategy looks like this:

1. Contribute pre-tax (traditional) during your highest-earning years.

2. Use early retirement years to complete Roth conversions at controlled, lower tax brackets.

Here’s why this approach often produces the best lifetime tax outcome.

Reason 1: Your Income Is Usually Highest During Working Years

For many Spokane families, peak working-year income pushes them into the 22%, 24%, or even 32% federal tax brackets. These are relatively high-income years, so the deduction you get from traditional contributions is especially valuable.

Paying Roth taxes today means voluntarily paying taxes in a high bracket, which is usually not ideal.

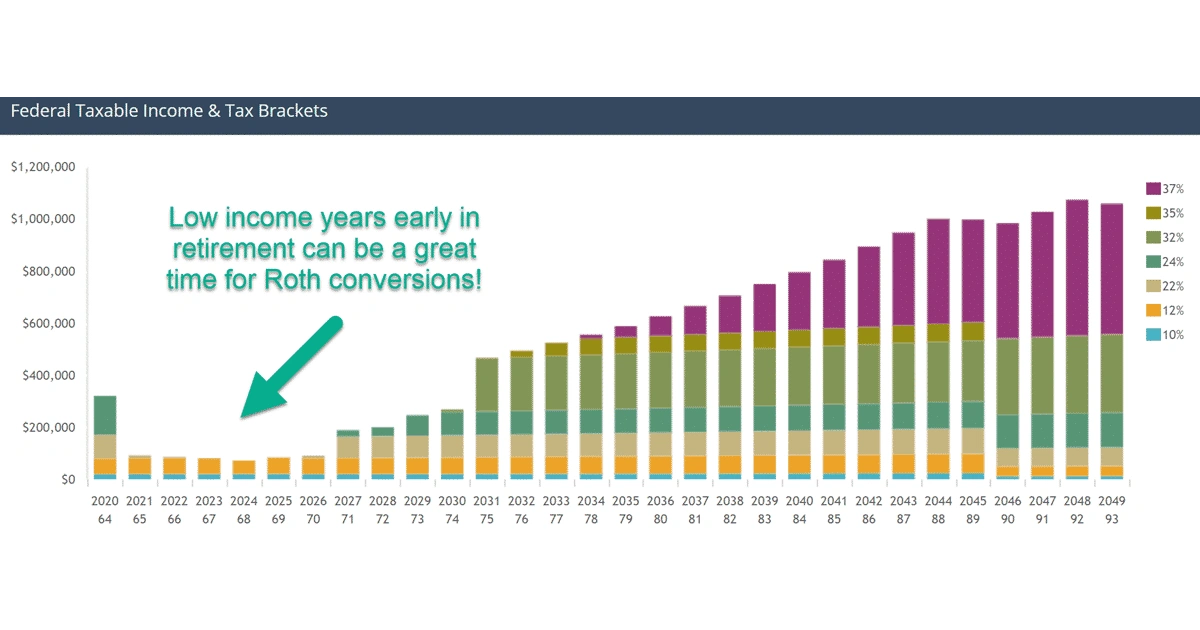

Reason 2: Retirement Often Comes With a Natural “Tax Valley”

Most retirees experience a window of time, often from retirement age until age 73 or 75 (when RMDs begin), where taxable income drops significantly.

During this window:

- Wages are gone

- Social Security may not have started yet

- Pensions may not have started or may be modest

- Deductions often remain similar

This creates what we refer to in retirement planning as a “tax valley”.

In this valley, your federal tax bracket may fall dramatically, often into the 10% or 12% ranges, even for high-net-worth retirees. Some years might even fall close to the 0% capital gains bracket.

This period of lower income is the ideal time to strategically complete Roth conversions.

Reason 3: Required Minimum Distributions (RMDs) Will Raise Your Income Later

This is one of the biggest reasons relying solely on traditional contributions without a conversion strategy can backfire.

Starting at age 73 (or 75 for some, depending on current law), the IRS forces you to begin taking RMDs from your traditional retirement accounts—whether you need the income or not.

If you’re like many Spokane retirees with $1–3 million saved, RMDs can:

- Push you into higher tax brackets

- Increase the taxation of Social Security benefits

- Reduce the flexibility of your retirement income strategy

- Accidentally leave your heirs with a large taxable inheritance to distribute within 10 years

RMDs are the IRS’s way of eventually collecting tax on traditional 401(k) and IRA balances. If you don’t plan ahead, specifically with Roth conversions, you may pay more over your lifetime than necessary.

Reason 4: Roth Conversions Can Dramatically Reduce the Tax Burden on Your Heirs

For Spokane retirees who want to leave a meaningful financial legacy, Roth conversions are not just about your own retirement—they’re about the total tax bill your wealth will face over multiple generations.

Under current IRS rules, most non-spouse beneficiaries (including your adult children) must withdraw all inherited IRA funds within 10 years. This applies to both traditional and Roth accounts, but the tax impact is vastly different.

Here’s the key consideration:

Your children will likely inherit your IRA during their highest-earning years, often in their 40s, 50s, when they are in much higher tax brackets than you are today.

That means:

- Every dollar they take from an inherited traditional IRA is taxed as ordinary income.

- They may be forced into the 32% or 35% brackets (or higher), even if they were previously in the 22% or 24% tier.

- The 10-year distribution rule compresses the timeline, removing their ability to stretch withdrawals over their lifetimes the way previous generations could.

In other words:

You may be unintentionally passing a large tax bomb to your children.

Many retirees focus only on minimizing their own taxes, but true financial planning must consider the total tax paid over the entire life of the account, not just during your own retirement.

This is where strategic Roth conversions can make a powerful difference.

Why?

- You may be able to convert those dollars in the 12% or 22% brackets during your early retirement years…

- …while your heirs may be forced to take withdrawals in the 32–37% brackets during their peak earning years.

A well-timed Roth conversion dramatically reduces the future tax burden on your beneficiaries because:

- Roth withdrawals for heirs are tax-free, even though they still must drain the account within 10 years.

- You “lock in” today’s tax rate instead of leaving your kids to pay taxes at much higher future rates.

- Your estate plan becomes more efficient, especially for families near the Washington State estate tax threshold.

So the question becomes:

Will your children pay more in taxes than you would pay today to convert to a Roth?

In many cases, the answer is yes, sometimes dramatically so.

This makes Roth conversions not only a retirement income strategy, but a multigenerational tax strategy, ensuring more of your wealth actually goes to your family instead of the IRS.

The Power of Strategic Roth Conversions in Retirement

Now let’s connect the dots:

Traditional contributions today → Roth conversions later → Lower lifetime taxes

Instead of paying taxes during high-income working years through Roth contributions, many retirees benefit more from:

1. Taking the tax deduction during peak earning years (traditional contribution)

2. Filling lower brackets in early retirement through deliberate Roth conversions

This strategy allows you to:

- Reduce future RMDs

- Lock in today’s historically low tax brackets

- Protect Social Security from unnecessary taxation

- Reduce future Medicare IRMAA penalties

- Give your heirs tax-free Roth assets

And when done correctly, you can often execute these conversions in the 12% or 22% brackets, much lower than the 24–32% brackets your contributions would have been taxed at during your working years.

For many Spokane retirees, that’s a substantial difference across a 20- to 30-year retirement.

A hypothetical Spokane Case Study: Traditional + Conversions vs. Roth Contributions

Let’s look at an example representative of many of the retirees we serve.

Meet Dave and Karen

- Ages 59 and 58

- Live in Spokane

- Dave will retire at 62

- Karen at 60

- Combined 401(k) savings: $1.6 million

- Currently in the 24% tax bracket

Scenario 1: They make Roth contributions during working years

They pay taxes now at 24% to fund Roth accounts.

Upon retirement, they have a mix of Roth and traditional accounts.

But when RMDs start, they still have:

- Around $1 million in traditional accounts

- RMDs estimated at $45–50k per year

- Forced income is pushing them into higher brackets later in retirement

Not terrible, but not optimal.

Scenario 2: They make traditional contributions now and complete Roth conversions later

Instead of paying 24% tax today on Roth contributions:

- They contribute pre-tax during working years

- They retire at 60–62

- They convert approximately $80k each year for 10 years before RMDs begin

- They keep conversions within the 12–22% brackets

- They dramatically reduce future RMDs

- They enter RMD age with over $1 million already converted to Roth

Outcome:

- Their lifetime tax bill was reduced by six figures.

- They enjoy more control over their income.

- RMDs drop to a fraction of what they would have been.

- Their heirs receive more tax-free assets.

This strategy is especially powerful when guided by a professional (e.g., a CPA or CFP® professional) who runs multi-year tax projections and integrates them with Social Security timing, pension choices, and estate planning considerations.

Why Roth Conversions Are Especially Valuable in Washington State

Washington State does not have an income tax, which means:

- Roth conversion taxes are federal only

- There is no additional state tax penalty for conversions

- You can convert significant amounts at a lower total cost than residents of other states

- The Washington State estate tax becomes a meaningful planning factor, and Roth assets can reduce taxable estate size depending on if you're using the account to pay for the tax.

For high-net-worth retirees in Spokane, this combination makes Roth conversions uniquely attractive.

When Roth Contributions Do Make Sense During Working Years

Even though traditional contributions plus Roth conversions are often the optimal route, there are absolutely scenarios where Roth contributions during working years are appropriate:

1. You expect to be in a significantly higher bracket later

For example, a young professional early in their career.

2. You’re in a very low bracket today

Many younger workers or part-time earners fall into this group.

3. You want tax diversification

Some clients simply prefer having both account types.

4. You value flexibility above strict tax optimization

Roth accounts offer unmatched flexibility later in life.

5. You are far below the Washington State estate tax threshold

Roth assets can still help but are not always necessary.

If you’re in your peak earning years and planning for retirement in Spokane within the next 5–10 years, these scenarios are less common—but not impossible.

The “Financial Planning Secret” Spokane Retirees Must Know

After years of helping Spokane retirees with seven-figure 401(k)s optimize their retirement income strategy, here’s the core insight:

The Roth vs. traditional decision isn’t really about contributions. It’s about long-term tax planning.

The typical contribution strategy looks at today’s tax bracket.

The optimal retirement strategy looks at:

- Today’s bracket

- Future brackets

- Social Security taxation

- Medicare IRMAA thresholds

- RMD impacts

- Heir tax implications

- Estate tax considerations

- Washington State tax environment

Simply choosing “Roth or traditional” today is a small part of a much larger picture.

How a Spokane Financial Advisor Can Help You Optimize This Decision

If you’re within 5–10 years of retirement, or already retired, the Roth vs. traditional choice should be part of a full retirement tax strategy.

As a Spokane financial advisor, here’s what we analyze for clients:

✔ Multi-year tax projections

Using advanced tax software to forecast brackets from age 55 to age 95.

✔ Social Security optimization

Matching conversion windows with Social Security timing.

✔ Pension integration

Particularly important for Spokane retirees who worked at Delta, the airlines, Providence, or local school districts.

✔ RMD reduction strategies

Building a conversion timeline that keeps future forced withdrawals low.

✔ Medicare IRMAA planning

Avoiding unexpected penalties due to poor conversion timing.

✔ Washington State estate tax planning

Structuring conversions to reduce exposure when net worth exceeds $2.193 million.

✔ Distribution strategies

Designing an income plan tailored to today’s market, your goals, and your tax situation.

This level of planning is what turns the Roth vs. traditional choice from a simple contribution question into a powerful retirement optimization strategy.

Final Thoughts: What Should You Do Right Now?

If you’re like many of the retirees we serve in Spokane, you may already have:

- The majority of your savings in traditional 401(k)s

- A high income during working years

- A desire to reduce RMDs later

- A goal of minimizing lifetime taxes and leaving more to your family

If that’s the case, the most effective strategy is often:

Traditional contributions today → Strategic Roth conversions in early retirement

This approach allows you to use the “tax valley” years to your advantage, lower your lifetime tax bill, reduce RMDs, and build a more flexible, tax-efficient retirement.

But every situation is unique, and taxes change frequently. The right answer depends on personalized planning.

If you want a customized analysis or a multi-year Roth conversion plan, reach out anytime. As a Spokane financial advisor and CFP®, helping retirees optimize this exact decision is one of the most valuable parts of our work.

Meet with our Spokane Financial Advisor today

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax and financial planning

Noah Schwab, CFP®, is a Spokane financial advisor specializing in helping retirees with tax-efficient retirement income strategies, Roth conversions, and estate planning. This article is for educational purposes only and should not be considered tax or legal advice.