How Much Can You Safely Withdraw From $1M?

If you have $1 million saved for retirement, a reasonable starting withdrawal range is often around 3% to 5% per year, or roughly $30,000 to $50,000 before taxes. But that is only a starting range, not a universal answer. Morningstar’s current retirement-income research places a baseline 30-year starting rate around 3.9% for retirees seeking steady, inflation-adjusted spending, while more flexible households may be able to start higher. The real answer depends on your age, Social Security timing, health risks, taxes, account mix, market conditions, and whether you can adjust spending over time. That is why a thoughtful Spokane Financial Advisor should treat this as retirement income planning, not just a percentage question.

A plain-English answer

For many retirees, $1 million may support about $30,000 to $50,000 a year from the portfolio as an initial planning range. A more conservative retiree with a long time horizon may lean toward the lower end. A retiree with flexibility, additional guaranteed income, or a shorter planning horizon may be comfortable higher. What matters most is not simply what you can withdraw, but what you can keep spending after taxes without taking unnecessary risk.

A safe withdrawal rate is best understood as a starting point for retirement withdrawals, not a promise. It should be coordinated with retirement income planning, tax-efficient retirement income, Social Security planning, and investment management. A withdrawal strategy that ignores those pieces can look fine on paper and still create problems in real life.

Why $1M does not create the same retirement income for every retiree

Two retirees can both have $1 million and still need very different withdrawal strategies.

A 62-year-old couple with no pension, high spending needs, and most assets in pre-tax accounts may need a more cautious starting withdrawal because their portfolio may need to last 30 years or more. A 74-year-old retiree with Social Security, a small pension, and a healthy Roth or brokerage balance may be able to draw more from the portfolio because the time horizon is shorter and the tax picture may be more flexible. The “right” withdrawal rate changes with time horizon, asset allocation, market conditions, inflation, and spending flexibility.

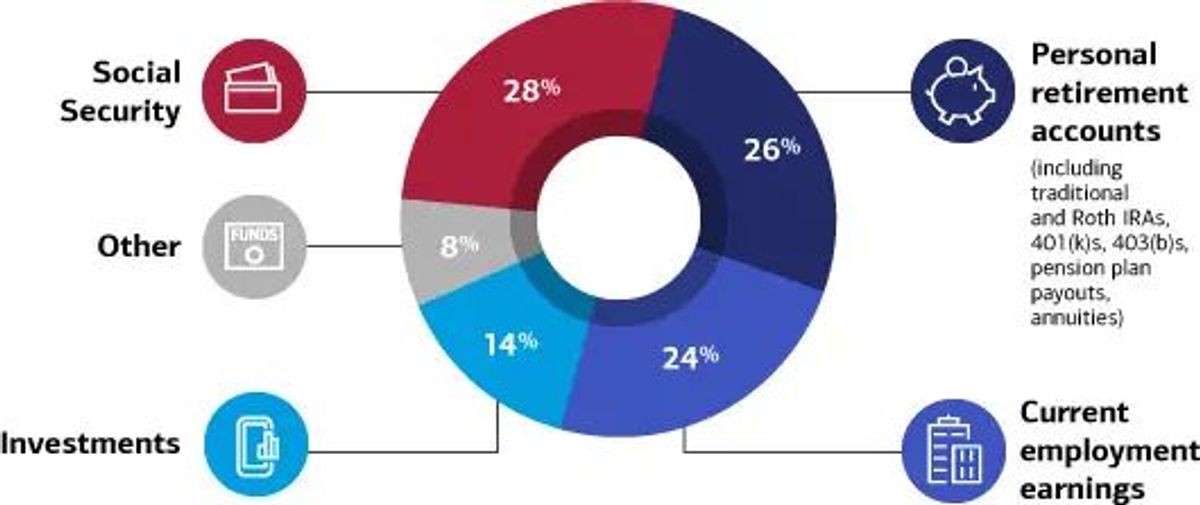

That is the core point many articles miss: $1M is an asset value, not an income guarantee. You have to take into account your retirement age, life expectancy, spending needs, taxes, guaranteed income, and legacy goals, because they all influence how much of that portfolio can be responsibly spent as retirement income.

The 4% rule is a starting point, not a retirement plan

The 4% rule remains useful because it gives people a clear frame of reference. On a $1 million portfolio, 4% means a first-year withdrawal of about $40,000.

But it is still just a rule of thumb. Morningstar’s more recent research estimated a baseline starting safe withdrawal rate of 3.9% for a 30-year retirement with inflation-adjusted spending, and it also found that retirees willing to accept some spending variability may be able to start closer to 6%. The key lesson is not that one number replaced another. It is that the “right” number depends on the retiree’s actual situation.

The 4% rule also does not answer several questions retirees actually care about:

- How much of that withdrawal will be lost to taxes?

- Should you claim Social Security at 62, full retirement age, or 70?

- What happens when required minimum distributions begin?

- How should you withdraw from taxable, tax-deferred, and tax-free accounts in the right order?

- How much spending can you protect if markets fall early in retirement?

That is why a rule of thumb can be helpful, but it is not a complete retirement withdrawal strategy.

What affects a safe withdrawal rate most

Retirement age and time horizon

In general, the earlier you retire, the more conservative your initial withdrawal rate may need to be. A retirement that could last 30 to 35 years places different demands on a portfolio than one expected to last 15 to 20 years. Older retirees with shorter time horizons can often spend more than the base case used for a 30-year retirement.

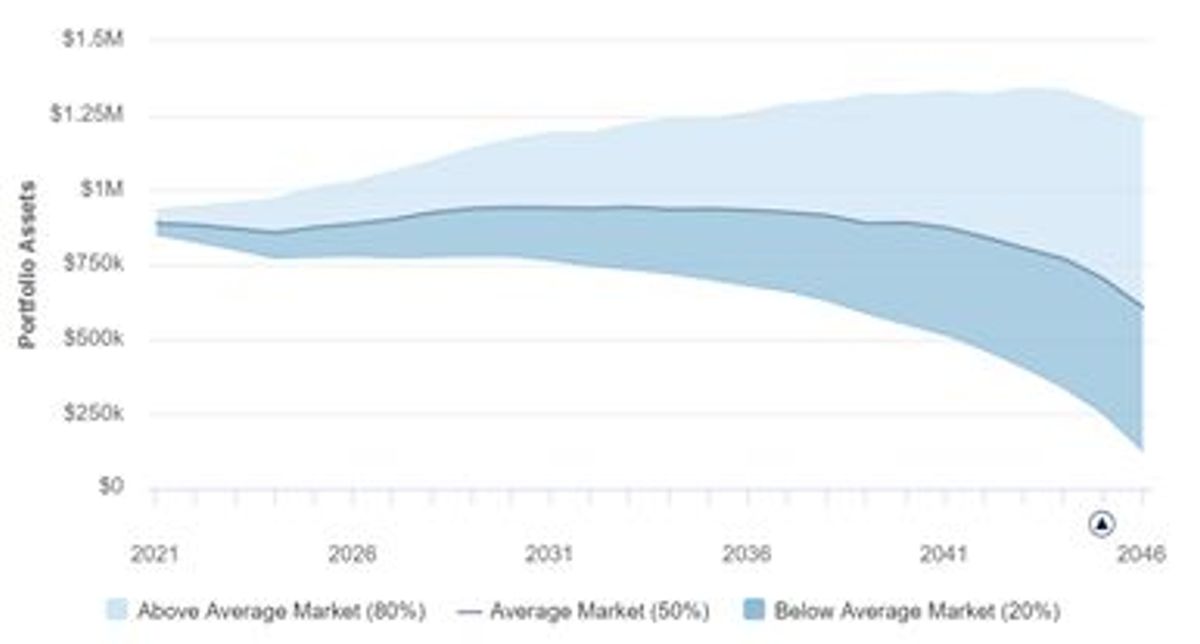

Inflation, market volatility, and sequence of returns risk

Two risks can cause real damage early in retirement: inflation and sequence of returns risk.

Inflation can steadily increase the amount you need to spend just to maintain the same lifestyle. Poor market returns early in retirement can also be especially damaging when you are taking withdrawals at the same time, a challenge often called sequence of returns risk. Studies have found that retirees who experience high inflation or weak returns in the early years of retirement are more likely to run down savings unless they are willing to adjust spending. That is why good financial planning is so valuable. Tools such as Monte Carlo analysis can help you test how a retirement income plan might perform across a range of market environments, including difficult “what if” scenarios.

Guaranteed income, flexibility, and legacy goals

A retiree whose essential expenses are largely covered by Social Security or a pension usually has more flexibility than someone relying almost entirely on the portfolio. The same is true for retirees who can reduce travel or gifting during weak market years. By contrast, someone who wants a substantial legacy for children or charity may intentionally choose a lower withdrawal rate. Delayed Social Security and flexible spending approaches tend to improve the sustainability of retirement income, though they may reduce amounts left for heirs.

Gross withdrawals are not the same as spendable retirement income

This is one of the most important distinctions in retirement planning.

A $40,000 withdrawal from a traditional IRA is generally not the same as $40,000 you can spend, because deductible contributions and earnings withdrawn from a traditional IRA are generally taxable. By contrast, qualified Roth IRA distributions are tax-free, and brokerage withdrawals may include a mix of basis, dividends, and capital gains rather than all ordinary income. That means two retirees withdrawing the exact same gross dollar amount may end up with very different net spending power.

This is where tax-efficient retirement income matters. A strong investment advisor should not be focused only on returns. They should help connect investment management to financial planning, withdrawal sequencing, and retirement tax planning so the portfolio supports the household’s actual spending life.

How Social Security, taxes, RMDs, and Roth conversions change the answer

Social Security planning matters

Social Security can dramatically change how much you need from the portfolio. The Social Security Administration says retirement benefits can begin as early as 62, but benefits are reduced if you start before full retirement age. If you wait until 70, your monthly benefit is higher because of delayed retirement credits, and there is no additional increase for waiting past 70. That makes Social Security timing one of the biggest levers in retirement income planning.

For many households, delaying Social Security can reduce pressure on the portfolio later in life, especially for the surviving spouse. But it usually requires careful coordination in the years before benefits begin.

RMDs can reshape your tax picture

The IRS has required minimum distributions generally begin at 73 for traditional IRAs and many employer retirement plans, though some workplace-plan participants can delay RMDs until retirement if they are not 5% owners. Roth IRAs do not require lifetime RMDs.

That matters because RMDs can force taxable withdrawals whether you need the cash or not. A retiree who looked very tax-efficient at 68 can look very different at 73 if large pre-tax balances begin pushing income higher.

Roth conversions can improve long-term flexibility

A Roth conversion does not create “free” money. The IRS says converting a traditional IRA to a Roth IRA causes taxation of untaxed amounts in the traditional IRA. But in the right years, Roth conversions can reduce future RMDs, improve tax flexibility later, and create a larger pool of tax-free assets for future spending or heirs.

This is also where Medicare planning comes in. Social Security explains that higher-income beneficiaries pay income-related monthly adjustment amounts for Part B and Part D premiums, and those premiums are based on MAGI from the tax return the government uses. In practice, that means large taxable-income years deserve careful planning, especially when you are weighing conversions, capital gains, or unusually large IRA withdrawals.

Two practical examples

Example 1: Long horizon, tax-heavy account mix

A married couple retires at 65 with $1 million, most of it in 401(k)s and traditional IRAs. They have no pension, want stable spending, and are thinking about delaying Social Security to 70.

For this couple, a starting portfolio withdrawal of around $35,000 to $40,000 may be more prudent than jumping to the high end of the range. They have a long time horizon, a high dependence on the portfolio, and most withdrawals will likely be taxed as ordinary income. Their plan may also include partial Roth conversions before RMD age to improve future tax flexibility.

Example 2: More guaranteed income, more flexibility

A 74-year-old retiree has $1 million split among a brokerage account, a Roth IRA, and a traditional IRA. Social Security plus a small pension already cover most core living expenses.

This retiree may be able to withdraw $40,000 to $50,000 from the portfolio in some years without taking the same level of risk as the first couple, especially if discretionary spending is flexible and the portfolio is not carrying the whole retirement. But the plan still needs to account for RMDs, taxes, and how much of the estate should remain for heirs.

The point of both examples is simple: the safe number is personal.

Common retirement income planning mistakes

A few mistakes show up again and again:

- Treating the 4% rule as a full plan instead of a starting benchmark.

- Focusing on gross withdrawals and ignoring after-tax spendable income.

- Claiming Social Security without looking at longevity, survivor income, and tax effects.

- Ignoring the window for Roth conversions before required minimum distributions begin.

- Keeping withdrawals rigid when markets fall, rather than adjusting spending when needed.

- Thinking retirement planning is only about investments, when it also touches taxes, Medicare, beneficiary designations, and estate planning.

Most retirement income problems are not caused by one catastrophic decision. They come from several smaller decisions that were never coordinated.

When a Spokane Financial Advisor can help

There is real value in speaking with a Spokane Financial Advisor when retirement income decisions start overlapping.

That is especially true if you:

- have $1 million or more spread across IRAs, Roth IRAs, brokerage accounts, and cash,

- are deciding when to start Social Security,

- want to compare portfolio withdrawals with partial Roth conversions,

- are worried about future RMDs or Medicare premium surprises,

- want coordinated financial planning, investment management, retirement tax planning, and estate planning.

A good fee-only, team-based advisor is not there to hand you a 1% fee and send you on your way. They help build a plan that aligns with your tax situation, spending priorities, and goals for the years ahead.

In the end, the safest answer to “How much can I withdraw from $1M?” is not one fixed dollar amount. It is a thoughtful range, tested against real life. That is the kind of work a steady Spokane Financial Advisor should be doing with you.

Frequently Asked Questions

How much income can $1 million generate in retirement?

A $1 million portfolio may support roughly $30,000 to $50,000 a year as a starting planning range, but the sustainable amount depends on time horizon, taxes, guaranteed income, spending flexibility, and market conditions. Research put a baseline 30-year starting rate at 3.9% for steady inflation-adjusted spending, while more flexible approaches may support a higher starting rate.

Is the 4% rule still a good rule?

It is still a useful benchmark, but not a complete retirement plan. It does not account for taxes, Social Security timing, RMDs, Roth conversions, or how much flexibility you have if markets fall.

How much can a conservative retiree withdraw from $1M?

A conservative retiree may start closer to 3%, especially with a long retirement horizon, high dependence on the portfolio, or a desire to avoid large spending changes. The right figure depends on the household, not just the portfolio size.

How much can I withdraw from $1M after taxes?

That depends on where the money comes from. Traditional IRA withdrawals are generally taxable, while qualified Roth IRA distributions are generally tax-free. Because of that, two retirees taking the same gross withdrawal can end up with different spendable income.

Do Social Security and RMDs change how much I can withdraw?

Yes. Social Security can reduce the amount your portfolio must provide, and delaying benefits until 70 can increase the monthly benefit. RMDs generally begin at age 73 for traditional retirement accounts and can force taxable withdrawals even if you do not need the cash.

Can Roth conversions help create safer retirement income?

They can, in the right situation. Roth conversions are taxable in the year of conversion, but they may reduce future RMDs and create more tax-free flexibility later. Because Medicare premium adjustments are tied to MAGI from your tax return, conversion years should be planned carefully.

What does sequence of returns risk mean in retirement?

It means bad market returns early in retirement can do more damage when you are also taking withdrawals. Poor early returns combined with ongoing withdrawals can permanently weaken a portfolio even if long-term average returns later improve.

Next Step

If you are trying to turn $1 million into reliable retirement income, the real question is not just “What percentage can I withdraw?” It is “How do I build a plan that fits my taxes, my accounts, my lifestyle, and my family?” A fee-only, team-based Spokane Financial Advisor can help you connect withdrawal strategy, Social Security planning, Roth conversions, investment management, and estate planning into one practical plan.

Talk with our Spokane Financial Advisor team

About the Author

Noah Schwab, CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax, and financial planning

Noah Schwab, CFP®, is a Spokane financial advisor specializing in helping retirees with tax-efficient retirement income strategies, Roth conversions, and estate planning. This article is for educational purposes only and should not be considered tax or legal advice.