What is a required minimum distribution?

Often referred to as an RMD, a required minimum distribution is an unavoidable withdrawal every year starting at age 72 from all tax-deferred accounts such as an IRA or 401k. Created by the government, this rule is designed to start bringing in taxes on those accounts.

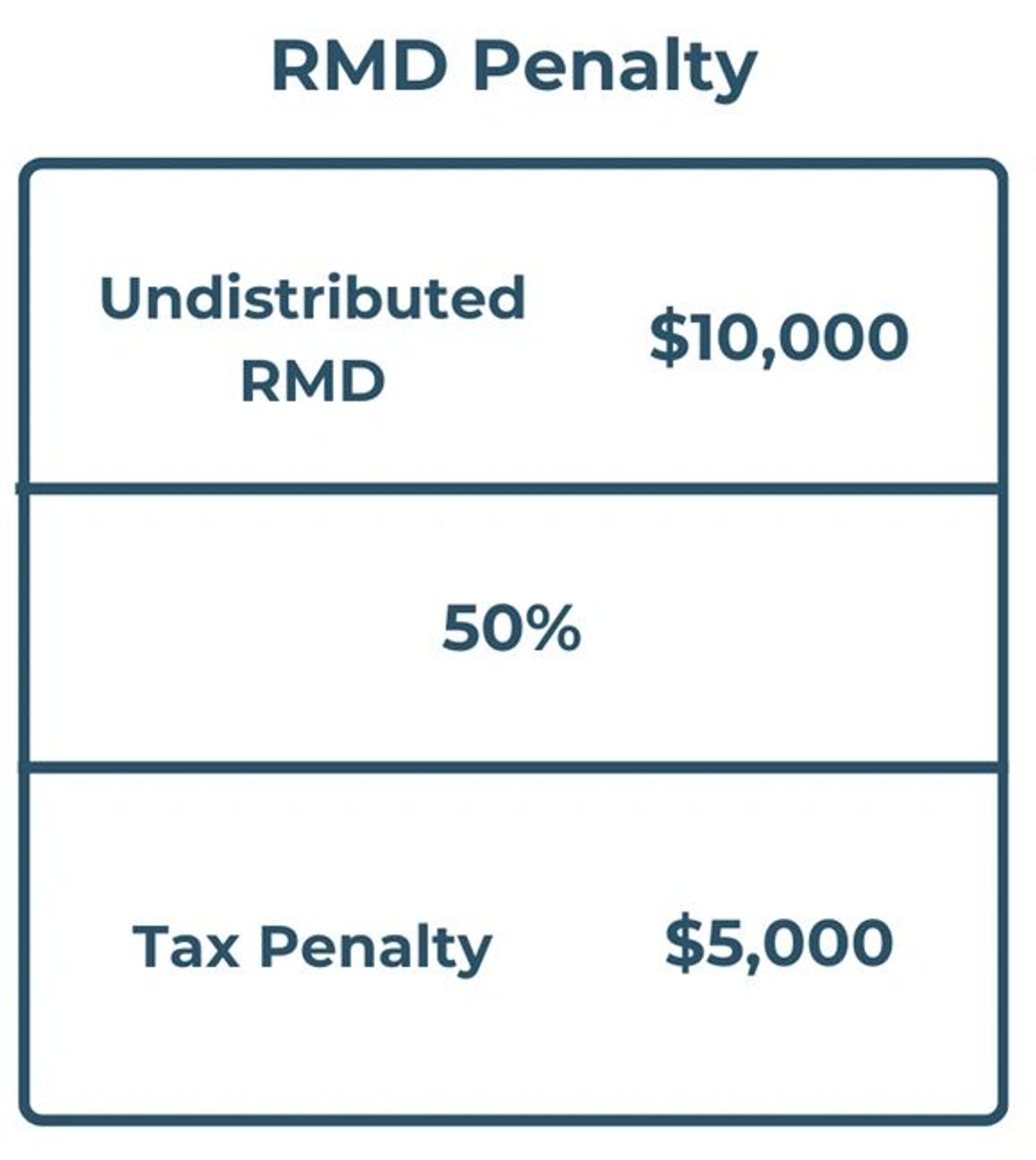

If someone forgets to take their required minimum distribution, they are penalized based on half the amount that wasn’t distributed.

For example, if someone was supposed to take $10,000 as an RMD and doesn’t, they would owe $5,000 in taxes

How is the distribution calculated?

The RMD amount is based on age and the value of all tax-deferred accounts at the beginning of the distribution year. As someone ages, the distribution percentage decreases. The full amount will never be required to be taken out.

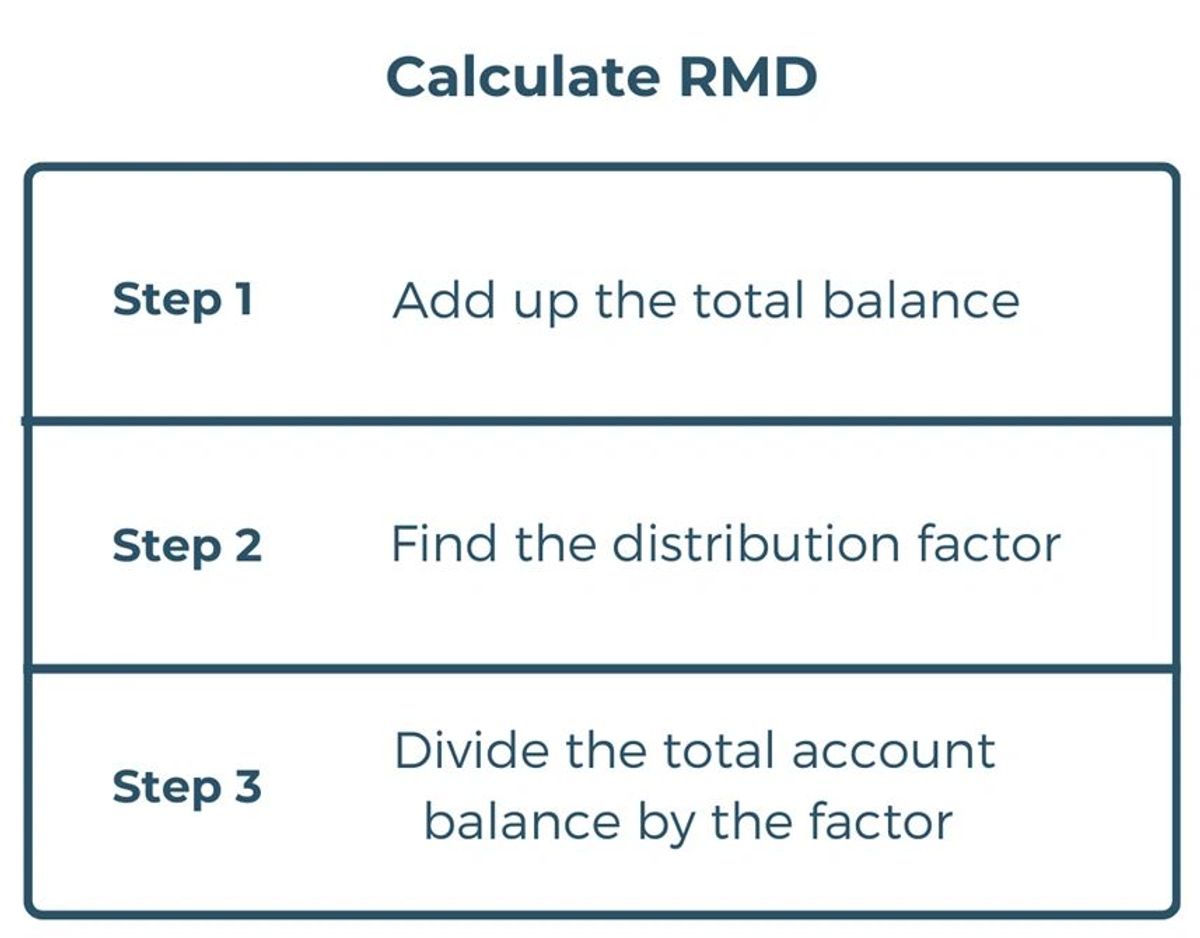

Step 1 Add up the total balance of all tax-deferred accounts as of December 31st of the previous year (traditional IRA, 401k, 403b, 457, SIMPLE IRA, SEP IRA). Do not include Roth or taxable accounts.

Step 2 Find the distribution factor based on your birthdate. It ranges from 1.9 up to 27.4. Use this website to find your factor.

Step 3 Divide the total balance by the distribution factor to calculate your RMD for that year.

If you are having trouble calculating this amount you can alternatively go to this government website and use their RMD calculator.

Four strategies to lower RMD taxes

1. Keep working

This is probably the least helpful method because most people don’t have the option or even want to work past age 72. Savers in a 401(k) who continue working past age 72 and don’t own 5% or more of the company can delay distributing from that 401(k) until they retire. But if there is an IRA or a past 401(k) from a previous employer, they will still be under the RMD rules.

2. Roth IRA conversion

Great to implement after you stop working and before age 72. For those years of low taxable income and sizeable investments in tax-deferred accounts, you have the option to pay the taxes and convert your funds into a Roth IRA. Not limited to any amount, this can be a great way for money to grow tax-free. This also lowers your RMD because the calculation doesn’t consider Roth IRAs. This powerful strategy can build long-term wealth for generations. Work with your financial advisor and CPA to strategize on what amount and the best method to do this.

3. Avoid the tactic of delaying your first distribution

In the year you turn age 72, you are allowed to avoid taking your first distribution until you file your taxes on April 15ththe next year. Some people see try and avoid as much tax in the current year and choose to do this. But by delaying your payment the first year, means that the next year will have two RMD’s which will be taxable. This could put you into a higher tax bracket and make the total tax bill higher over those two years. This method depends on your personal tax situation. Consult with your CPA and financial advisor before you decide to do this.

4. Use Qualified Charitable Distributions

QCDs are one of the best tax savings for those who have RMDs. If someone is already giving to a charity like a church or non-profit, this can save you thousands. The tax code allows contributions of up to $100,000 from tax-deferred accounts each year to a nonprofit organization. The amount given is not taxable income. This means you can satisfy your RMD for the year and would have no additional income if you were to give it to charity.

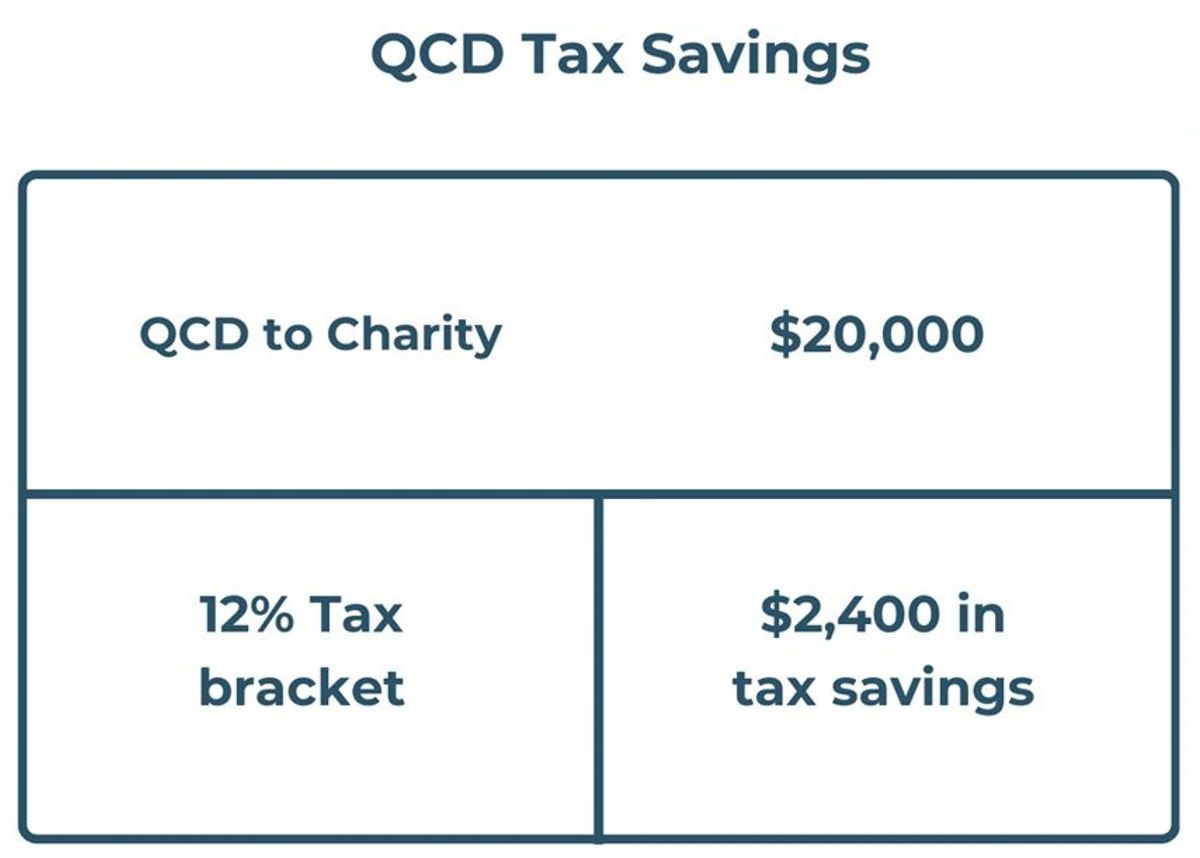

For example, $20,000 given to charity using a QCD while in the 12% tax bracket will save $2,400 in taxes.

Other required distributions- Inherited IRAs:

With an inherited IRA, there will also be required distributions but you can't utilize QCDs with this type of account. Distribution rules depend on when the account was inherited. If inherited after the SECURE Act in December 2019 then generally the account must be distributed entirely at the owner's discretion within 10 years from the date of death. A popular strategy is to spread the distribution evenly over those years to lessen the tax impact. But there could be an opportunity for better tax savings if a lower income tax year exists. Check with your CPA and financial advisor to determine the best strategy.

About the Author

Noah Schwab CFP® is a financial planner in Spokane, Washington who specializes in helping small business owners with retirement plans and personal finances.

Resources:

Government website to calculate RMD: https://www.investor.gov/financial-tools-calculators/calculators/required-minimum-distribution-calculator

RMD distribution table for 2022: https://www.bankrate.com/retirement/ira-rmd-table/#:~:text=To%20calculate%20your%20required%20minimum,calculate%20your%20RMD%20every%20year.

RMD’s: https://www.investopedia.com/terms/r/requiredminimumdistribution.asp

Inherited IRA’s: https://www.investopedia.com/articles/personal-finance/102815/rules-rmds-ira-beneficiaries.asp