Understanding QCDs: The Ultimate Guide for Retirees

Written by Noah Schwab, CFP®, a financial advisor in Spokane specializing in Roth Conversion for retirees with over $1M+ in a 401k

If you’re a retiree with a traditional IRA, you may be looking for ways to minimize your taxes while supporting causes you care about. One powerful and often overlooked tool is the Qualified Charitable Distribution (QCD). As a Spokane financial advisor, I help retirees leverage QCDs to reduce taxable income, manage and avoid required minimum taxes on distributions (RMDs), and achieve charitable giving goals. In this guide, you’ll learn everything you need to know about QCDs, from eligibility and tax benefits to strategic planning and common mistakes.

What is a Qualified Charitable Distribution (QCD)?

A QCD is a direct transfer of funds from your IRA to a qualified charity. The main benefit is that the distribution counts toward your Required Minimum Distribution (RMD) for the year, but it is excluded from taxable income. This makes QCDs a valuable tool for retirees who want to limit the tax impact of RMDs on income taxes while supporting charitable causes.

Who is Eligible for a QCD?

To make a QCD, you must meet the following requirements:

- Age Requirement: You must be 70½ or older at the time of the distribution.

- Eligible Accounts: Only distributions from traditional IRAs, including inactive SEP or SIMPLE IRAs, qualify. QCDs do not apply to 401(k)s or other employer-sponsored retirement plans, although funds can often be rolled into an IRA first.

- Eligible Charities: Funds must go to a qualified 501(c)(3) public charity. Donor-advised funds, private foundations, and supporting organizations do not qualify.

For more information, you can visit the IRS Publication 590-B

How Do QCDs Work?

Executing a QCD is straightforward but requires careful planning:

- Request a Distribution from Your IRA Custodian: Specify that you want to make a QCD and the amount to transfer directly to the charity.

- Direct Transfer is Critical: Funds must be sent directly from your IRA to the charity. Withdrawing the money yourself first disqualifies it as a QCD.

- Tax Reporting: You’ll receive Form 1099-R showing the distribution. The QCD is excluded from taxable income but should still be reported correctly on your tax return.

- RMD Counting: QCDs count toward your RMD, reducing your taxable income while fulfilling the IRS requirement.

This technique applies to traditional IRAs, not to Roth IRAs. For more information on the differences between a traditional IRA VS Roth IRA

The Benefits of QCDs for Spokane Retirees

QCDs offer multiple advantages that make them a valuable tool for retirement planning:

1. Reduce Taxable Income

RMDs from a traditional IRA are fully taxable as ordinary income. High-income retirees may face higher federal tax brackets, increased Medicare premiums (read article on IRMAA explained), and more taxation on Social Security benefits. QCDs allow you to:

- Fulfill RMD requirements without increasing taxable income

- Lower adjusted gross income (AGI) to minimize Social Security and Medicare taxation. Check out this article on how to maximize Social Security.

2. Support Charitable Giving

QCDs let you give to charity in a tax-efficient way. Because the distribution is excluded from income, the charity receives the full donation. Benefits include:

- Supporting causes you care about consistently

- Reducing the tax burden on other retirement income

- Avoiding reliance on cash flow for charitable contributions

3. Reduce Medicare Premiums

Since QCDs lower AGI, they can reduce Medicare Part B and Part D premiums, also known as IRMAA. Even modest reductions in AGI can lead to meaningful savings over time. Check this out if you need to sign up for Medicare at 65, and learn how to avoid penalties.

4. Avoid Standard Deduction Limitations

For retirees taking the standard deduction, traditional charitable donations may provide little tax benefit. QCDs, however, reduce taxable income directly, regardless of whether you itemize deductions.

How Much Can You Give Through a QCD?

You can contribute up to $111,000 per person per year through a QCD (in 2026). Married couples with separate IRAs can each give $111,000, effectively doubling the limit. Coordinate your QCD with your RMD: if your RMD is $20,000 and you donate $15,000, the remaining $5,000 will still be taxable.

Strategic QCD Planning

To maximize the benefits of QCDs, consider these strategies:

1. Timing Your QCD

- Complete QCDs by December 31 to count toward that year’s RMD

- If making multiple QCDs in a year, confirm with your IRA custodian to avoid processing errors

2. Combining with Other Tax Planning Tools

QCDs are most effective when paired with other strategies:

- Roth Conversions: Offset additional taxable income from Roth conversions. Check out this article for Roth conversion tax strategies for Spokane retirees.

- Charitable Giving Ladder: Spread donations across multiple years to smooth tax liability

- Medicare and Social Security Planning: Reduce AGI to prevent higher Medicare premiums and taxable Social Security

3. Coordinating with Estate Planning

QCDs can also support estate planning goals:

- Reduce the taxable portion of your IRA for beneficiaries

- Preserve other assets for heirs while supporting charities

- Combine with donor-advised fund strategies (QCDs cannot go directly into these funds)

Common Mistakes to Avoid with QCDs

- Using an ineligible retirement account like a 401(k)

- Sending distributions to yourself first instead of directly to the charity

- Exceeding the $111,000 annual limit per person

- Donating to non-qualified charities (donor-advised funds, private foundations). For more details, check out this article I wrote on donor-advised funds, explained by a Spokane financial advisor.

- Failing to report the QCD properly on your tax return

Example: How a QCD Can Save Taxes

Scenario: Susan, 73, has an IRA with a $50,000 RMD and wants to donate $25,000 to charity.

Without QCD:

- Withdraws $50,000; fully taxable

- Donates $25,000, and doesn't benefit from an itemized deduction

With QCD:

- Directly transfers $25,000 from IRA to charity

- Only $25,000 of the RMD is taxable

- Reduces income taxes by $3,000 ($25,000 QCD X 12% tax bracket) while still fulfilling her charitable goals

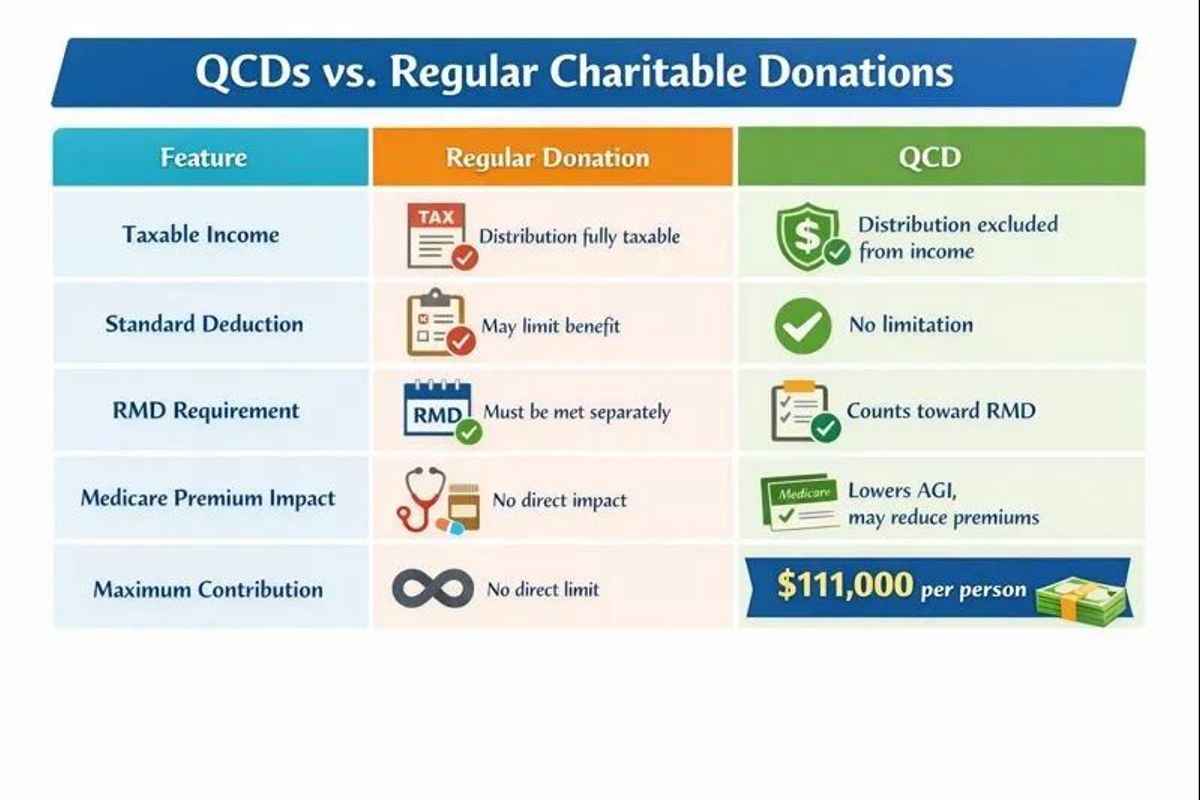

QCDs vs. Regular Charitable Donations

QCDs are often a more efficient strategy than taking a taxable IRA distribution and then making a regular charitable donation. In many cases, a QCD is one of the most powerful charitable giving tools available to retirees.

Key Takeaways

- QCDs are a tax-smart way to give and satisfy RMDs

- Only available at age 70½+, from IRAs, and must be direct transfers to eligible charities

- Maximum annual QCD: $111,000 per person

- Reduces taxable income, Medicare premiums, and Social Security taxation

- Work with a Spokane financial advisor to coordinate QCDs with Roth conversions, estate planning, and charitable goals

QCD Frequently Asked Questions (FAQ)

What is a Qualified Charitable Distribution (QCD)?

A QCD is a direct transfer from your IRA to a qualified charity, counting toward your RMD but excluded from taxable income.

Who is eligible to make a QCD?

You must be 70½+ and use a traditional, SEP, or SIMPLE IRA. 401(k)s are not eligible unless rolled into an IRA.

How much can I contribute?

Up to $111,000 per person per year. Married couples can combine for $222,000.

Which charities qualify?

Eligible 501(c)(3) public charities. Donor-advised funds and private foundations do not qualify.

Do QCDs count toward my RMD?

Yes, they fully satisfy RMD requirements while lowering taxable income.

How is a QCD reported on taxes?

Form 1099-R is issued, and the distribution is reported as non-taxable on your tax return.

Can I donate more than my RMD?

Yes, up to $111,000. Excess reduces taxable income but does not count toward future RMDs.

Can I use a Roth IRA?

No. Roth IRA distributions are generally tax-free, so QCDs are unnecessary.

Can I donate to a donor-advised fund?

No. Only eligible charities qualify.

How can QCDs affect Medicare and Social Security taxes?

By lowering AGI, QCDs can reduce taxable Social Security and Medicare premiums.

Should I work with a financial advisor?

Yes. A Spokane financial advisor can coordinate QCDs with RMDs, Roth conversions, charitable goals, and estate planning.

Common Mistakes to Avoid

- Indirect transfers

- Using ineligible accounts

- Exceeding limits

- Donating to non-qualified organizations

Are you looking for a Spokane financial advisor who understands QCDs, RMDs, and tax-efficient retirement planning? Schedule a call with us to see how your IRA can work for both your retirement and your favorite causes. Or if you want to check out more great financial advisors, see our updated list of the best 5 financial advisors in Spokane.

Working With a Spokane Financial Advisor

As a Spokane financial advisor, I help retirees navigate RMDs, QCDs, and tax-efficient retirement planning. Planning your QCD strategy includes:

- Reviewing IRA accounts and RMD requirements

- Confirming eligible charities

- Timing distributions for tax efficiency

- Integrating QCDs with Roth conversions and estate plans

If you want to explore how QCDs can reduce taxes and support your favorite causes, contact a Spokane financial advisor today.

Bottom Line: QCDs are a highly effective strategy for managing RMDs, reducing taxable income, and supporting charitable giving. Understanding eligibility, contribution limits, and tax implications ensures you maximize benefits.

Talk with our Spokane Financial Advisor team

About the Author

Noah Schwab, CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax, and financial planning

Noah Schwab, CFP®, is a Spokane financial advisor specializing in helping retirees with tax-efficient retirement income strategies, Roth conversions, and estate planning. This article is for educational purposes only and should not be considered tax or legal advice.