The Retirement Tax Surprise Many Spokane Retirees Experience

Let’s start with a situation I see fairly often. You’ve worked for decades, saved diligently in your 401(k), and finally retire. Social Security begins, your income plan is in place, and life slows down a bit. Then tax season rolls around. You sit down with your accountant and hear something unexpected: Part of your Social Security benefits is taxable.

For many retirees, this comes as a real surprise. After all, you paid into Social Security your entire career. It’s reasonable to assume those benefits would come back tax-free. But here’s where many retirees get surprised. Once you start taking withdrawals from your 401(k) or IRA, those withdrawals can push your income high enough that the IRS begins taxing part of your Social Security benefits.

As a Spokane financial advisor who works with retirees every day, I see this happen regularly, especially for people who have $1 million or more saved in retirement accounts. The good news is that once you understand how Social Security taxation works, there are strategies that may help reduce the impact.

Let’s walk through how it works.

Why Retirees With Large 401(k)s Often Pay Tax on Social Security

If you spent most of your career saving in a traditional 401(k), you probably benefited from years of tax deferral. That’s great during your working years. But in retirement, those same accounts can create a new tax dynamic. Here’s why: Withdrawals from a traditional 401(k) or IRA count as taxable income. If you're approaching retirement and wondering what your options are with a 401(k) when you retire, it’s important to understand how withdrawals can affect both your taxes and Social Security benefits..

When that income gets combined with other retirement income sources, like Social Security, pensions, or investment income, it can push your total income high enough that your Social Security benefits become partially taxable.

This is something many Spokane retirees don’t realize until retirement actually begins. The more income you generate from tax-deferred accounts, the more likely it becomes that a portion of your Social Security benefits will be taxed. That’s why retirement tax planning becomes especially important for retirees with large retirement accounts. A knowledgeable Spokane financial advisor can help coordinate withdrawals, Roth conversions, and Social Security timing to help manage taxes over time.

How Social Security Is Taxed (Simple Explanation)

One of the most common questions retirees ask is: “How much of my Social Security can be taxed?”The answer depends on your income. The IRS allows up to 85% of your Social Security benefits to become taxable income.

Now this part is important. That doesn’t mean Social Security is taxed at 85%. Instead, it means up to 85% of your benefits may be included in your taxable income calculation. Let’s say you receive $40,000 per year in Social Security benefits.

Depending on your income, as much as $34,000 of that amount could be counted as taxable income. Your normal tax bracket would then apply to that portion. Whether this happens depends on a calculation called provisional income.

What Is Provisional Income? (The Formula That Determines Social Security Taxes)

Provisional income is the formula the IRS uses to determine whether your Social Security benefits are taxable. The calculation includes three main things:

- Your adjusted gross income (not including Social Security)

- Any tax-free interest, such as municipal bond income

- 50% of your Social Security benefits

- Put simply: Provisional Income = Other Income + Half of Social Security

Let’s walk through a quick example. Suppose a retired Spokane couple has:

- $60,000 in 401(k) withdrawals

- $40,000 in Social Security benefits

- Calculation: $20,000 (half of Social Security) + $60,000 AGI = provisional income of $80,000

That number determines whether their Social Security benefits become taxable. This is the step where many retirees first realize how retirement income sources interact with each other.

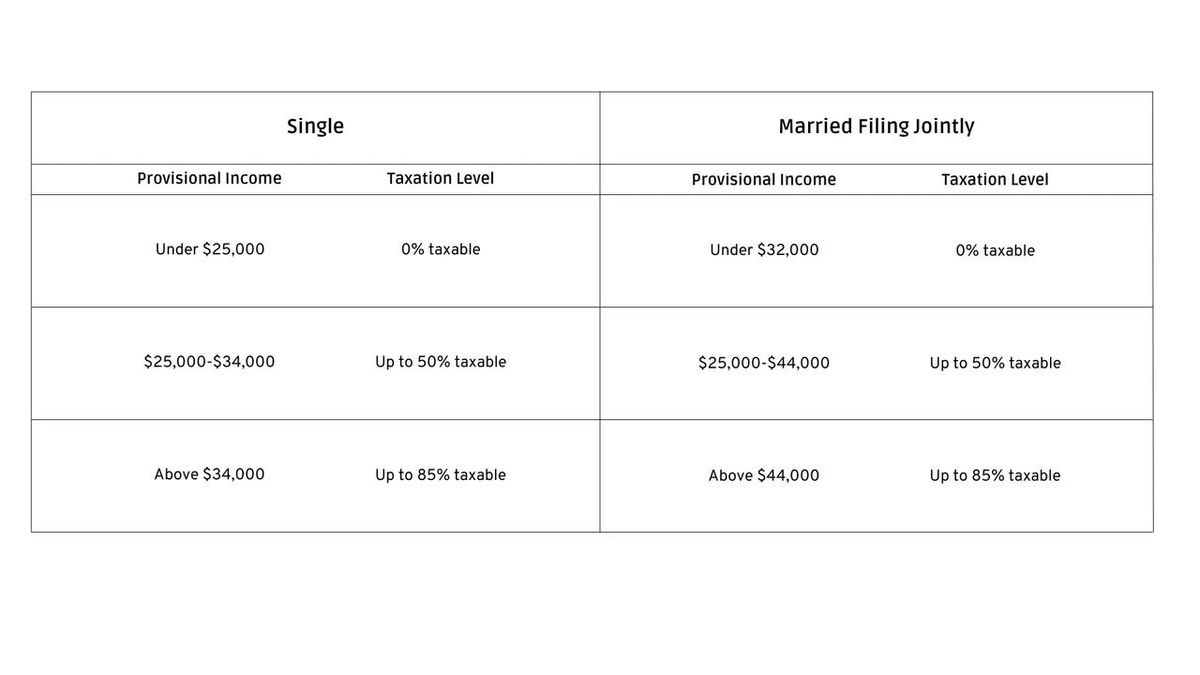

Social Security Tax Thresholds (2025 Rules)

The IRS uses income thresholds to determine how much of your Social Security benefits become taxable. The chart below shows when Social Security benefits may become taxable based on your provisional income.

Here’s another detail many retirees find surprising. These thresholds haven’t been adjusted for inflation since they were introduced decades ago. As incomes have risen over time, more and more retirees now find themselves paying tax on Social Security benefits.

Why 401(k) Withdrawals Increase Social Security Taxes

Now let’s connect the dots. When you withdraw money from a traditional 401(k), the IRS counts that withdrawal as ordinary income. That income increases your provisional income, which can push more of your Social Security benefits into the taxable range. Here’s where things get a little tricky. Sometimes a $1 withdrawal from a 401(k) can cause more than $1 of taxable income to appear on your tax return.

Why?

Because that withdrawal can cause a larger portion of your Social Security benefits to become taxable at the same time. Financial planners sometimes call this the “Social Security tax torpedo.” This is why thoughtful retirement tax planning can make a meaningful difference over time.

Strategies to Reduce Taxes on Social Security Benefits

While it’s not always possible to avoid Social Security taxes entirely, there are several strategies that may help reduce them. Let’s walk through a few common ones.

1. Roth Conversions Before Required Minimum Distributions

One of the most powerful tools in retirement tax planning is a Roth conversion strategy. A Roth conversion moves money from a traditional retirement account into a Roth IRA. You pay taxes on the amount converted today, but future withdrawals may be tax-free.

Here’s the key advantage. Withdrawals from Roth accounts do not increase provisional income. That means they typically do not cause more Social Security to become taxable. Many retirees consider Roth conversions during the years between retirement and Required Minimum Distributions (RMDs). This window can provide an opportunity to reduce future taxes.

2. Create Tax Diversification in Retirement

Another important concept is tax diversification. Here's the three tax categories:

- Tax-deferred accounts (401(k), traditional IRA)

- Tax-free accounts (Roth IRA)

- Taxable investment accounts

Understanding the differences between a traditional IRA and Roth IRA can help retirees create better tax diversification in retirement. When retirees have money across multiple tax categories, they have more flexibility when planning withdrawals. For example, if withdrawing from a 401(k) would push Social Security into a higher tax range, you might instead withdraw from a Roth account. That flexibility can make a meaningful difference in retirement.

3. Use Strategic Withdrawal Planning

The order in which you withdraw money from retirement accounts can significantly affect your taxes. Taxes on investment income can also play a role, especially when considering how capital gains tax works in retirement. Many retirees assume the strategy is simple, just withdraw from the 401(k) as needed. But sometimes a better approach might involve:

- drawing down tax-deferred accounts earlier

- performing partial Roth conversions

- using taxable brokerage accounts strategically

Each situation is unique. This is where working with a Spokane financial advisor who specializes in retirement tax planning can be valuable.

4. Consider the Timing of Social Security Benefits

The age at which you begin Social Security can also influence your tax strategy. Some retirees delay Social Security for a few years after retiring. Why? Because that window can allow them to:

- perform Roth conversions

- reduce future required distributions

- manage taxable income more efficiently

This approach isn’t right for everyone, but for retirees with large retirement accounts, it can sometimes help reduce lifetime taxes.

Example: How a Spokane Couple Triggered Social Security Taxes

Let’s walk through an example that reflects what many retirees experience. Tom and Linda retire in Spokane at age 67. Their financial picture looks like this:

- $1.3 million in a 401(k)

- $48,000 per year in Social Security benefits

- $20,000 annual pension

They decide to withdraw $70,000 per year from their 401(k). Their provisional income would look roughly like this:

- $70,000 (401k withdrawal)

- $20,000 (pension)

- $24,000 (half of Social Security)

- Total provisional income: $114,000 ($70,000 + $20,000 + $24,000)

At this income level, 85% of their Social Security benefits become taxable. Now imagine if Tom and Linda had performed Roth conversions during the early years of retirement. Reducing their future 401(k) withdrawals could potentially lower their provisional income and reduce Social Security taxation later. If you’d like to see how retirement tax planning works in real life, you can read this retirement planning case study showing how a Spokane couple approached their retirement strategy.

Frequently Asked Questions About Social Security Taxes

Do all retirees pay tax on Social Security?

- No.

- If your income stays below the IRS thresholds, your Social Security benefits may not be taxable. However, retirees with pensions or significant 401(k) withdrawals often cross those thresholds.

Does Washington State tax Social Security benefits?

- No.

- Washington State does not tax Social Security income. However, Social Security benefits may still be subject to federal income tax depending on your income.

Can Roth conversions reduce Social Security taxes?

- In some cases, yes.

- Roth conversions can reduce future withdrawals from tax-deferred accounts, which may lower provisional income later in retirement.

Do Required Minimum Distributions increase Social Security taxation?

- They can.

- Once RMDs begin (currently age 73), required withdrawals from retirement accounts increase taxable income. That additional income may cause more Social Security benefits to become taxable.

Why Retirement Tax Planning Matters

During your working years, the focus is usually on saving as much as possible. But once retirement begins, the focus shifts to how to withdraw money efficiently. For retirees who leave the workforce before age 65, income planning can also affect healthcare costs when retiring before Medicare and using ACA health insurance. Without proactive planning, retirees may face:

- higher tax brackets

- increased Social Security taxation

- larger Required Minimum Distributions

- higher Medicare premiums

That’s why retirement tax planning has become such an important part of financial planning today. Working with a Spokane financial advisor who focuses on tax planning for retirees can help coordinate withdrawals, Roth conversions, and Social Security decisions to potentially reduce lifetime taxes.

Talk With a Spokane Financial Advisor About Your Retirement Tax Plan

If you have $1 million or more saved in a 401(k), it may be worth taking a closer look at how taxes could affect your retirement income. Small adjustments, like strategic Roth conversions or thoughtful withdrawal planning can sometimes make a meaningful difference over time. An experienced Spokane financial advisor can help you:

- understand how Social Security may be taxed

- evaluate Roth conversion opportunities

- create a tax-efficient withdrawal strategy

- reduce the impact of Required Minimum Distributions

If you’d like to review your retirement tax strategy, the first step is simply a conversation. Many retirees find that proactive planning today can lead to lower taxes and greater flexibility throughout retirement.

Talk with our Spokane Financial Advisor team

About the Author

Noah Schwab, CFP® is a financial advisor in Spokane, Washington, helping retirees with $ 1M+ maximize their 401(k) with Roth conversions and tax strategies.

- No commissions or insurance

- Investment management, tax, and financial planning

Noah Schwab, CFP®, is a Spokane financial advisor specializing in helping retirees with tax-efficient retirement income strategies, Roth conversions, and estate planning. This article is for educational purposes only and should not be considered tax or legal advice.