Thank you to everyone for reading our blog. We've had great feedback and are excited that people are interested in what we say. Today's blog post focuses on avoiding taxes on retirement accounts. Everyone needs to know this BEFORE entering retirement.

Owners of tax-deferred accounts like a 401k, IRA, 403(b), or 401(a) must take a minimum amount (RMD) each year starting at age 73. A tax-deferred account means you've delayed paying taxes, so this excludes any Roth accounts or a brokerage account. Once you take money out of the tax-deferred account, it's considered income. For example, if you distribute $5,000 from your IRA, $5,000 of your income will show up on your taxes for that year. Today, I spill CFP ® 's secrets on reducing taxes and, in one strategy, completely avoiding taxes.

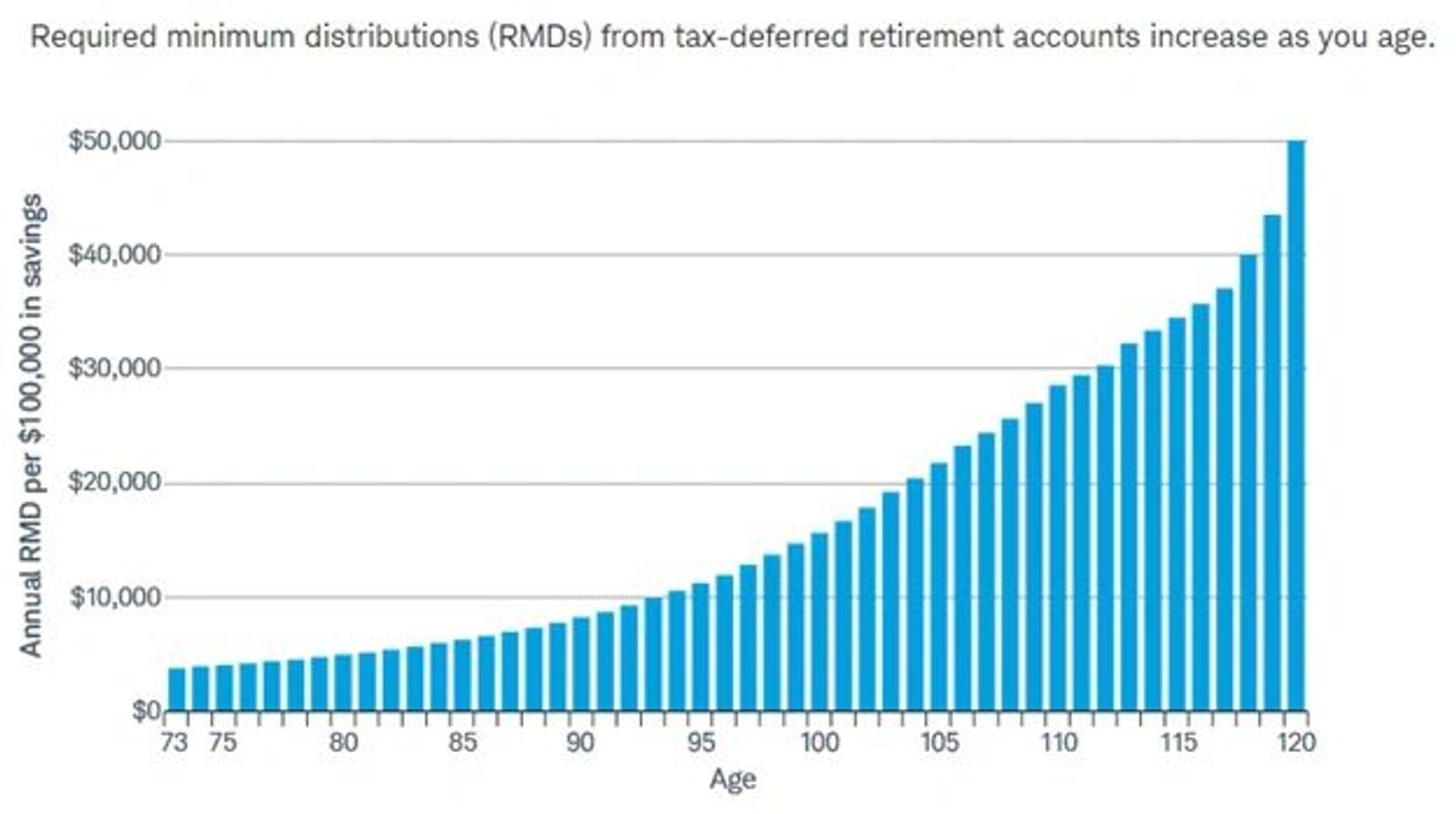

How an RMD is Calculated

For younger people, this RMD age rule changes from 73 to 75 in 2033 (9 years from now). Note that tax-deferred accounts only have one owner. A couple will have two separate RMDs and calculations if they each own tax-deferred accounts. The RMD each year is determined by someone's age and the value of the accounts. The older someone is, the higher percentage is used, and the larger the account's value, the more will be required to be removed. This is nitty-gritty:

- Add the balance of all tax-deferred retirement accounts in one person's name as of December 31 of the previous year.

- Find the distribution period corresponding to the age you'll turn this year.

- Divide the account balance by the distribution period to determine your RMD for each account. The IRS permits you to aggregate your RMD amounts for all your IRAs and withdraw the total from a single IRA.

If you feel overwhelmed by this calculation, use an RMD calculator. Check this online tool: RMD calculator.

Avoid Penalties

If someone fails to take an RMD, you'll owe a penalty of 25% of the amount you should have withdrawn. However, it will drop to 10% if the mistake is corrected within two years. Once you reach the RMD age, there are fewer options to lower your tax bill or avoid taxes, so planning your tax strategy ahead is important.

Don’t Wait

One strategy is to start withdrawing funds from tax-deferred accounts at age 59½—generally your earliest opportunity without incurring a 10% penalty. The goal is to withdraw not so much that you edge yourself into a higher tax bracket. This strategy will reduce the value of your tax-deferred accounts because your RMD is calculated based on the value of your accounts. Your forced future RMDs will be smaller, and the goal is for them to avoid pushing your income into a higher tax bracket at that time.

Also, don't wait to take your RMD once you turn 73. Even though a rule allows you to delay taking the first RMD until you file taxes for that year, it's usually more helpful to take an RMD in the first year, turning 73. The alternative is postponing your first distribution until April 1 of the following year, forcing a double distribution in that year, and you may enter a higher tax bracket. A reason for delaying your first year's RMD is if you have a significant one-time tax bill, for example, selling a home or business. If you turn 73 this year, you can postpone your first distribution until April 1, 2025. But, for all years following the first year, the RMD deadline is December 31.

Qualified Charitable Distribution

This is the only way to avoid paying the tax completely. This strategy starts at age 70½. It's one of the most powerful strategies, especially for those who already give to charity. There is a way to reduce or entirely satisfy your RMD and avoid income taxes by doing a qualified charitable distribution (QCD). This is where money is transferred directly from an IRA to a qualified charitable organization like a nonprofit or church. Unlike RMDs, QCDs are not taxable, and each individual (married or single) can donate up to $105,000 for tax year 2024 from their IRA. You may also direct a one-time, $53,000 QCD to a charitable remainder trust or charitable gift annuity in 2024, which also counts toward your annual limit.

To do the QCD, you must give from an IRA. Your IRA custodian must transfer the funds directly—and only to a 501(c)(3) organization. You can't contribute to a donor-advised fund. You can't claim the QCD as a charitable deduction, but the huge benefit is that the distribution doesn't count as taxable income, which is a more significant tax benefit.

A QCD makes sense, especially if someone values giving to a nonprofit or charity. If you give out your IRA, you can reduce your estate, which is helpful if it's subject to Washington State estate tax. Also, utilizing and reducing your tax-deferred accounts like an IRA helps your heirs avoid being forced to take distributions (income) in the 10 years after your death, which is typically their highest income tax bracket. We strategize and set up our clients with a checkbook they can write to many charities annually. A QCD doesn't have to all go to the same charity, and it could be only a portion of their RMD if they want to take the rest to pay for living expenses.

*Tip* You can also QCD from an inherited IRA if you are at least 70.5.

Roth Conversions

Another great strategy is Roth conversions. This involves converting tax-deferred investments (IRA) to a Roth account exempting from Required Minimum Distributions (RMDs). There are several situations where a conversion may make sense:

- You believe you'll be in a higher bracket when you withdraw the money from your IRA (RMD or otherwise).

- You want to manage or reduce distributions once you hit your RMD age.

- You want to leave your heirs an income tax-free asset because Roth withdrawals aren't subject to income tax, assuming you've held the account for at least five years.

With a Roth conversion, you can convert any amount in a year. The only catch is that you'll owe ordinary income tax on the converted funds. If you can, it's to your advantage to pay any tax liability with other taxable account assets, such as cash from your bank account, to maximize the amount converted.

A Roth IRA conversion is usually the most advantageous during your initial retirement years when RMDs haven't begun. You will be in a much lower tax bracket, which is a great time to accelerate income at a lower rate. If you're already receiving retirement benefits, just be aware that the converted funds will increase your taxable income, potentially causing taxes on your Social Security benefits and Medicare costs to rise.

Remember the five-year rule if you're considering a Roth IRA conversion. This rule states that your Roth IRA must be open for at least five years to avoid a 10% tax penalty on withdrawing earnings. If you're opening a Roth IRA for the first time to receive converted traditional IRA funds, ensure you won't need to withdraw the earnings for at least five years. This usually isn't a problem because most of the account will be contributions within the first 5 years of the account being opened. Each Roth conversion restarts the five-year rule, but it's just on the funds that were converted that year.

If you're considering a Roth conversion, check out this Schwab Roth conversion calculator or talk to one of our Spokane financial advisors.

Beware Medicare Premiums

Only applicable for those age 65 and older, when calculating Roth conversions, it's important to know how your income affects your Medicare premiums. IRMAA is a very long acronym that is a surcharge for people with income above certain amounts to pay in addition to their Medicare Part B and Part D premiums. IRMAA is calculated every year based on two years prior.

If you have a one-time high-income event that pushes you into a higher income bracket, we recommend clients set up an appointment with the Spokane local Social Security office and explain why their income was high that year. For future years, if income falls, the surcharge should be lower. Double-check to make sure it’s correct.

Working Longer

By continuing to work past 73 and contributing to your work's 401k, the IRS allows you to delay taking RMDs. The catch is that it only applies to that 401k at your work. If you have a 401(k) from a previous employer or a traditional IRA, then the RMD rule applies.

This is a much less common solution because it requires a huge sacrifice. Unless someone is already desiring to work because of what they do, I don't often recommend it to clients.

QLAC

A qualified longevity annuity contract (QLAC) is a deferred annuity funded with an investment from a qualified retirement plan or an individual retirement account (IRA). A QLAC provides guaranteed monthly payments that begin after the specified annuity starting date and is exempt from RMD rules until the owner reaches age 85. Individuals are allowed to move $200,000 to a QLAC annually.

QLACs aren’t included in the RMD calculation, which effectively reduces the RMD. The funds within the QLAC can be delayed until age 85, which will be taxed as income. I don't recommend this to clients a lot of the time because insurance products have high fees, so you must compare the tax savings versus the fees and performance. Our advantage at Stewardship Concepts is that we don't sell any insurance products. Even though we could make more money, we believe in being unbiased with our recommendations, and by not receiving compensation, we eliminate this problem.

RMD Cash Strategy

In a declining market, many who need funds from their IRAs to pay expenses could be forced to sell securities at a loss to satisfy their RMD.

Keeping enough money in safe, low-risk investments, such as money market or cash, to cover your RMD is a great idea. If, for some reason, you don’t have sufficient funds in liquid accounts to fulfill your obligation, you may want to consider making what’s known as an in-kind distribution. With in-kind distribution, you arrange to transfer stock or mutual fund shares from your IRA to a taxable account, so you won’t have to sell your investments.

The IRS will tax the value of the shares as income. If you do this, ensure the value is equivalent to your RMD. The in-kind distribution is valued at the price of the shares at the market close on the day of the transfer. This maneuver won’t lower taxes on your RMD, but it will allow you to avoid selling investments at a loss. If you do an in-kind distribution, remember there won't be any tax withholding, so set aside cash for the tax bill when you file.

In Conclusion

Thank you for reading! This blog post was much longer and more in-depth than our average post. I didn't expect to write this much, but I shouldn't be too surprised because it is a complicated topic. Everyone's RMD strategy is different, and there is no template. Depending on where you live, your goals, needs, and the type of assets owed, your plan will differ. My advice for everyone is to start this process before you are forced to take RMDs because some of the most helpful planning techniques start before turning age 73. If you have questions, meet with one of our financial advisors to explore the best RMD tax strategy for you.

We have the capacity to help more people. To introduce us to someone, please share our website.

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington, specializing in helping couples with 401k five years from retirement.

- Fiduciary. No commission, no products

- Investment management and financial planning

Resources: