Inflation and Sequence Risk

Two of the most overlooked risks to retirement are inflation and sequence risk. Inflation is a popular term, but few have heard about sequence risk.

I’ll define both, give examples, and tell you how to protect your retirement against them.

My wife Jenny and I experienced inflation on our recent road trip to the Grand Canyon. The biggest shock on our trip was seeing $7.79 for a gallon of gas at Mono Lake, CA.

Luckily, we were able to wait and fill up our tank at the next gas station, paying over $6 a gallon.

Inflation is the value of a currency decreases while prices increase.

Example: When gas rises from $3.92 to $4.92 a gallon, it costs more for the same amount of gas - meaning every dollar you own is now worth less.

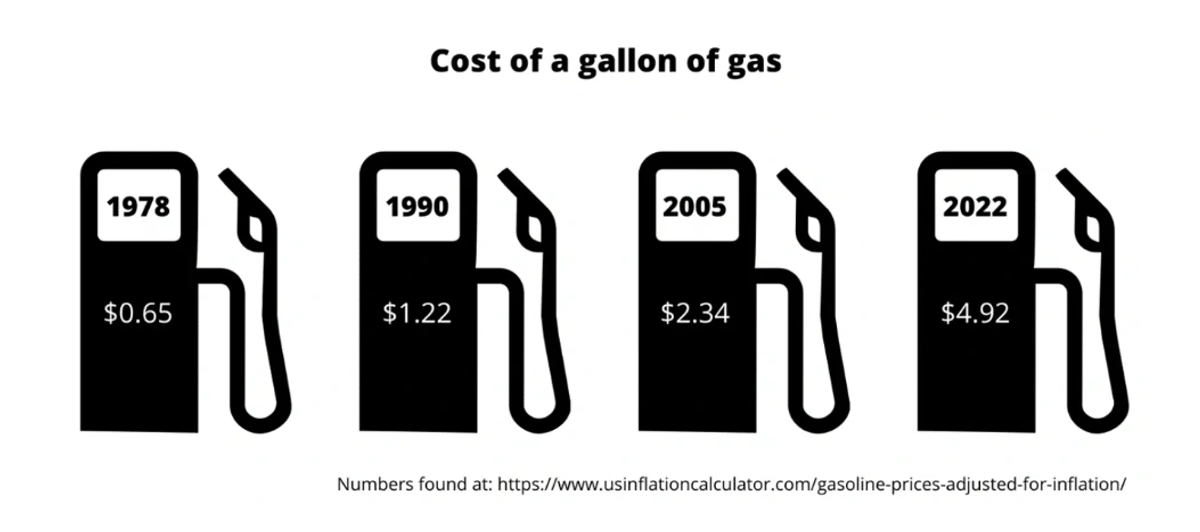

The cost of a gallon of gas just over 40 years ago was $0.65. If the same trend continues, it will eventually be about $25 per gallon in 30 years.

Future gas prices may lead to scary numbers, but not all inflation is bad. Inflation fuels higher valuations for stocks and other assets.

The government’s annual target is 2% inflation which helps our economy by encouraging spending and lowering the impact of our debt.

Savers that keep their savings in cash are getting hurt right now in two ways. Cash is horrible with inflation and great when there are high-interest rates. Right now, we have high inflation and low-interest rates.

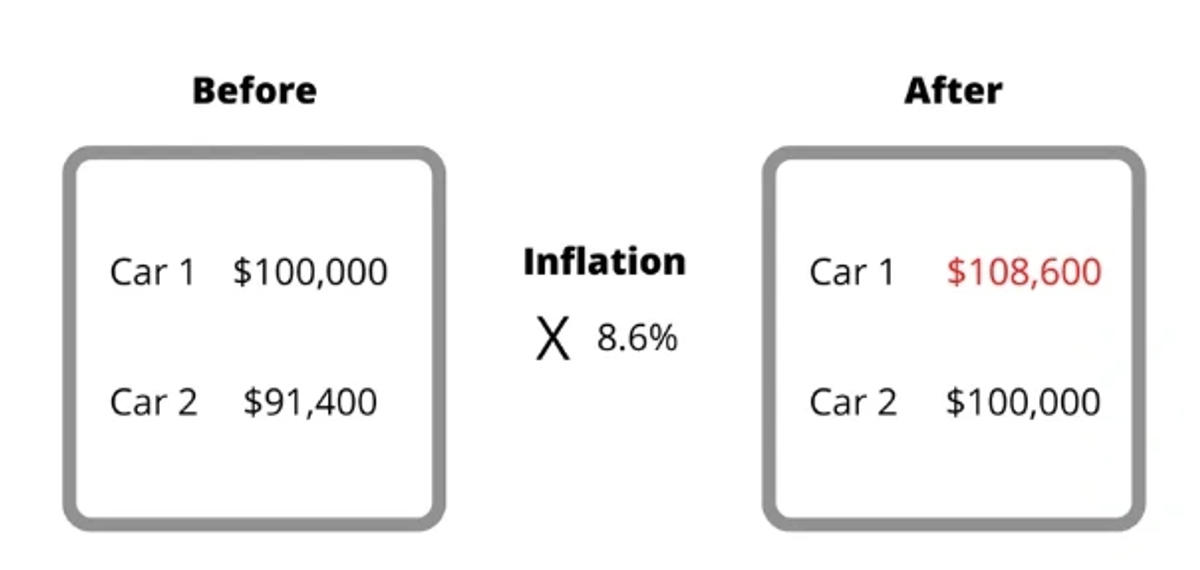

In our low-interest rate environment, savers get almost nothing in return for their savings. The real pain for savers comes with 2022’s inflation rate of 8.6%. Everything costs more.

With inflation, cash is worth less because you can buy fewer goods with the same amount of money. If someone had $100,000 saved, with 8.6% inflation, the following year the same amount of money would have the purchasing power of $91,400.

This is significant looking at retirement because every year inflation grows at a higher-than-average inflation rate, people’s historical data that they use for their financial plan becomes irrelevant.

People that were on track to retirement could no longer be. It’s important to review your financial plan when there are years of low market returns or high levels of inflation.

How to protect against inflation

Prepare

- Make sure your current and future budget has margin to absorb future inflation.

- Overestimate inflation when planning your retirement budget. Don’t pick the current year’s inflation - use a rate above the 30-year historical average (2.47%). We use 3% for our financial projections

Store cash in higher yield alternatives to a traditional savings account.

- High-yield saving accounts are typically offered by digital banks, such as Ally Bank. They can pass on the savings that they get from not having a brick-and-mortar store by offering higher interest rates.

- Money market accounts are another safe, liquid investment that can be used for higher yield. However, they may require more work to transfer money when a need arises.

Buy inflation-linked bonds

- Series I-bonds are government savings bonds that give interest plus an inflation rate. These bonds are limited to $10,000 a year per person and must be redeemed by the government. You can’t cash them in within 1 year and you are penalized with three months’ worth of interest if redeemed within 5 years.

- Treasury Inflation-Protected Securities (TIPS) are safe government bonds where the principal is adjusted for inflation. TIPS offer less inflation protection than I-bonds but are convenient because they typically can be used in an investment portfolio with no penalties for selling.

Protect your assets

- The price of stocks rises because the company metrics increase. For example, higher gas prices translate to bigger profits and a higher business valuation. Maintaining a portion of your wealth in stocks is a way to maintain protection against inflation.

- Real estate can be a great inflation hedge. Personally owning income-producing real estate or indirectly through REITs in your investment portfolio are great diversifiers.

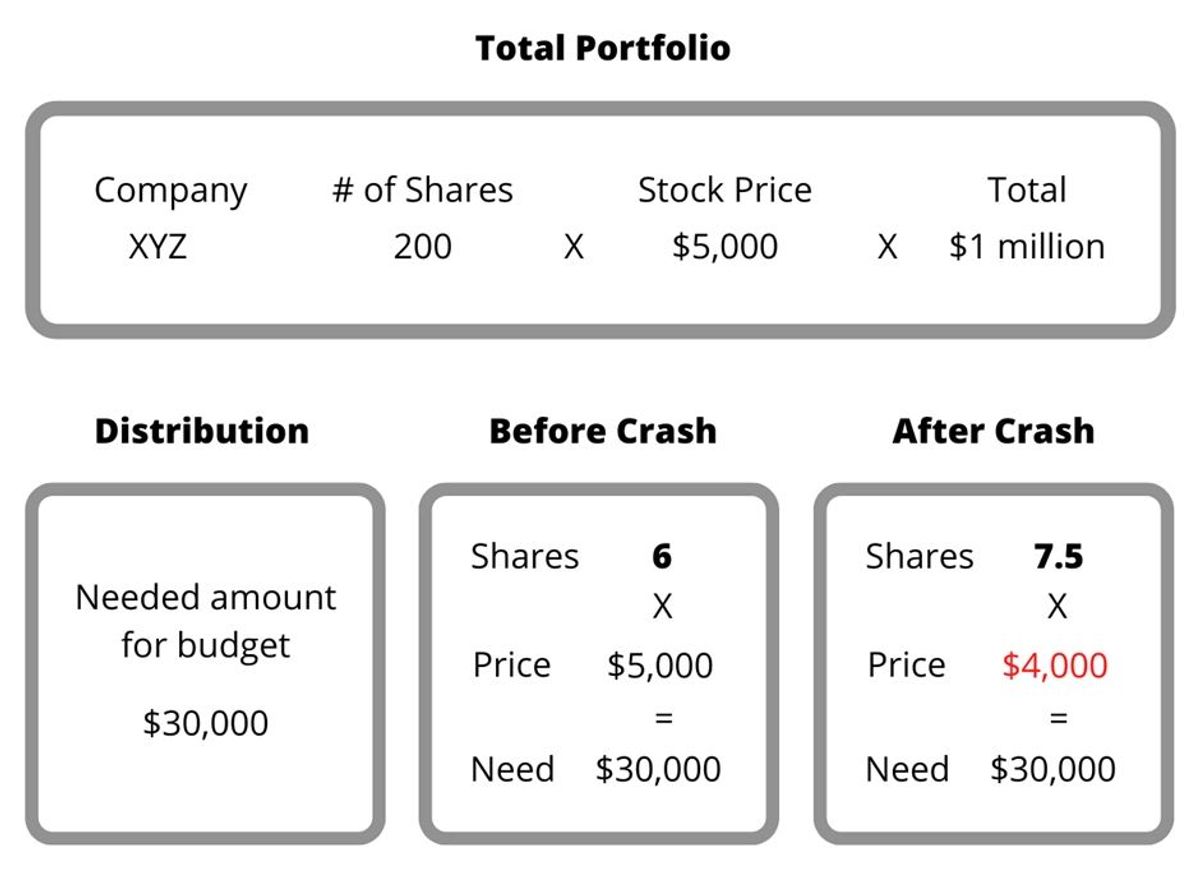

Sequence risk is the danger of taking investment withdrawals during a decline in the market. If you need $30,000 per year and the total value of your portfolio drops, you must sell a bigger slice of your investment “pie” to cover the need because your pie is now smaller.

What this means is that sequence risk hurts retirees because if your portfolio drops in value before you sell shares, you will lose out on the potential market rebound on the additional stocks sold.

Example: You need $30,000 a year. You have 200 shares of XYZ company worth $5,000 each for a total of $1 million dollars. To cover your need, you will have to sell 6 shares of XYZ for $30,000. But if the stock drops by 20% to $4,000, you will have to sell 1.5 more shares of XYZ to cover the same $30,000 need.

This hurts your portfolio because you have fewer shares of company XYZ to participate in the market rebound that typically follows a pullback.

How to protect against sequence risk

Lower distributions during market pullbacks

- Postpone vacations, gifting, and big purchases

- Reduce spending.

Keep two years of expenses in cash

- This allows you to wait for a market rebound instead of being forced to sell investments during a pullback.

Have a diversified portfolio.

- Avoid large concentrations in a few stocks.

- Invest in quality companies that have a long track record for stocks and bonds.

- Utilize safer investments - like bonds.

- Incorporate less stock correlated asset classes like gold, other commodities, and real estate.

We will never escape inflation and sequence risk entirely. But through prudent planning, we can lessen their impact on retirement. I believe being a good steward is an important and complicated task that takes a team - we can help.

As an advisor, I specialize in helping small business owners save time so they can do more of what is really important.

About the Author

Noah Schwab CFP® is afinancial planner in Spokane, Washington who specializes in helping small business owners with retirement plans and personal finances.

Learn more:

Our website: https://scfinancials.com/

Inflation: https://www.investopedia.com/terms/i/inflation.asp

Series I bond: https://www.investopedia.com/terms/s/seriesibond.asp

TIPS: https://www.investopedia.com/terms/t/tips.asp

High yield savings: https://www.nerdwallet.com/best/banking/high-yield-online-savings-accounts