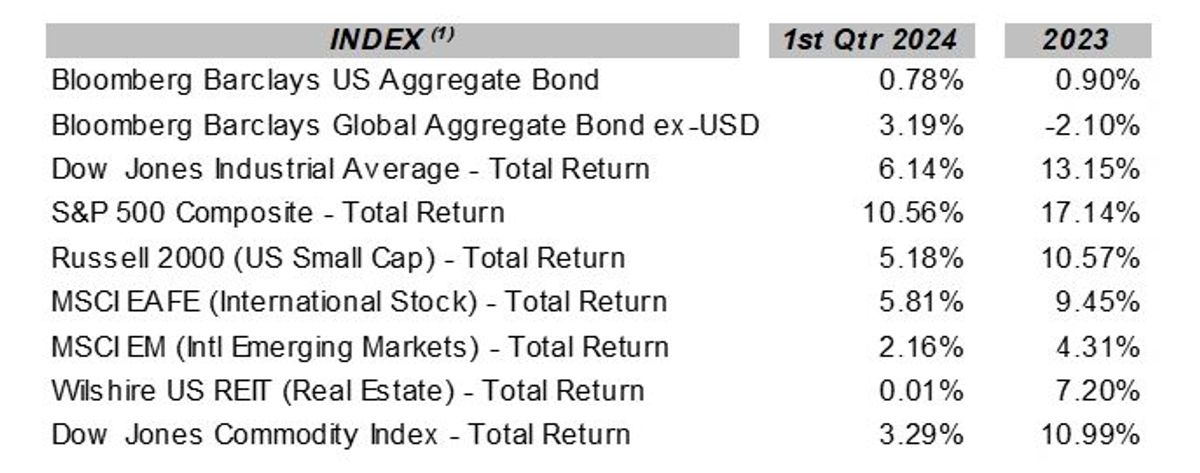

Performance

2024 started with a bang, continuing the stock rally from the fourth quarter of 2023, adding to returns. This first quarter was one of the strongest first quarters since 2019. Looking at the market in 2023, we saw a concerning trend where the seven largest companies making up roughly 30% of the S&P 500 (Microsoft, Apple, Amazon, Nvidia, Google, Meta, and Tesla) drove much of the return in that index. Their performance was fueled by an overcorrection in 2022 and a tailwind of the revolutionary technology- artificial intelligence.

AI

This technology has been around for a long time. AI is used in many products that you've used for a while, from Google Maps to spellcheck. AI drives tangible revenues and is a bright light for companies utilizing technology. The reason why this technology has impacted companies now is because it's now more accessible than ever before to the average consumer. It's not only large companies that can implement AI technology. One revolutionary AI adoption this past year was Chat GPT, which gives consumers free access to a generative AI model allowing users to input commands like: "Write a thank you card," to which Chat GPT responds with three high-quality paragraphs of a well-thought-out thank you card in seconds. This technology will drive profitability and change industries over the next decade.

Mega Cap Trend

An encouraging piece of in this first quarter is broader participation of S&P 500 companies in the overall returns of the index. Which begins to reduce the impact and concentration of the already high valuation in the seven largest names mentioned above. We've also seen the earnings of most of the S&P 500 companies recover, which matches their growing stock price. We'll have to see if this trend persists in the future.

Election Year

That's right, it's been four years, and it's time. An election year is always a top concern. One statistic that I like to draw attention to is the historical average returns during an election year. The S&P 500 has positive returns 83% of the time in an election year, regardless of which party won. Even in an election year, it's important to stay invested. As money managers, we realize that many more factors than political ones affect our economy, like the market cycle, inflation, interest rates, valuations, and earnings. Often, legislation doesn't immediately impact the economy; it usually takes years to see its full effect. This was not the case during Covid, which had a massive instant and lingering economic impact.

Lingering Covid

In previous quarterly commentaries, Wyn mentioned the fiscal problems created in response to Covid. Our economy was in a car crash because the global economy was wholly shut down. The government gave us a huge morphine shot to negate the effects of the car crash. Our economy experienced massive stimulus through unprecedented additions to the US money supply and drastic cuts in the Fed fund rate. The prolonged effects of this massive stimulus are slowly making their way out of our financial system but continue to make it difficult to predict a recession. Only time will tell if future policies allow a natural course correction to reflect more historical market cycles.

Recession?

Due to the lingering monetary and fiscal effects of Covid on our economy, it's been challenging for economic analysts to predict when/if a recession will happen. It's been over two years since we first heard analysts predicting that we are entering a recession, but we've failed to see it happen. One way the Covid response has made it difficult to predict a recession is the surprising strength of the financial balance sheet of the average consumer. Due to government stimulus checks, the average American's balance sheet has been able to weather inflation, pay for higher prices, and keep driving our economy. If there wasn’t as much money circulating in our economy combined with wage growth, then inflation and higher interest rates would have hurt the consumer sooner. As the consumer's balance sheet begins to weaken, the likelihood of a recession will increase. One indication that this is beginning to occur is the increase in credit card debt, indicating that the consumer needs to tap credit reserves to make ends meet. We agree with the analysts predicting a mild recession in the latter half of this year. However, the timing of this recession hinges on inflation and interest rates.

Inflation & interest rates

Inflation and the Fed's fund rate are critical components for our economy in 2024. If inflation is stubborn for the rest of the year, we could see higher interest rates for longer and a higher employment rate, which could lead to downward pressure on stock prices. Inflation has dropped since mid-2022, when the inflation rate peaked at 9.1%, falling to 3.2% in February 2024. However, reducing inflation has become more challenging in the present quarter as the headline CPI rate has risen slightly. Overall, we continue to see a slight downward trend in inflation. We are closely monitoring this statistic because if inflation rises, it will change how the Fed reacts. Chairman Jerome Powell has stated that the Fed will do whatever it takes to lower the inflation rate to its 2.0% target, even if it leads to a recession and higher unemployment. So far, our economy has absorbed the effects of higher interest rates and has been resilient. Stock prices have risen so far in anticipation of rate cuts later this year. Which the Fed confirmed this past Wednesdaywhen it announced three rate cuts of 0.25% each in 2024. Whether or not these rate cuts happen as announced remains to be seen.

Looking forward

As Wyn mentioned in the last quarterly commentary, we continue to navigate our portfolios in unprecedented and uncertain times. In his Monday Morning Outlook, Brian Wesbury, the Chief Economist for First Trust Advisors, talked about how "The US has moved from a simple Keynesian-type model to what we call ’State-Run Capitalism’." The long-term government trajectory is one of our long-term concerns when discussing living in unprecedented times. In preparation for this year, we are continuing to extend bond duration to lock in higher yields for longer, as we believe we’ve seen a peak in yields. Even though we've experienced a stock rally in this first quarter, we expect more volatility and a decline as we enter a recession. We continue to hedge against volatility for equities and lean towards large cap, quality, and dividends. As we enter this year, we utilize active ETFs (Exchange-Traded Funds) as a tax-efficient vehicle for many investments. ETFs have lower costs and better tax advantages over individual stocks, bonds, and mutual funds. If you're wondering about where to get started with investing, check out the 10 steps to start investing.

Please reach out if you have any questions concerning any portion of this report. If you're looking for a financial advisor near you, check out the guide to the best 5 Spokane Financial Advisors for 2024.

About the Author

Noah Schwab CFP® is a financial advisor in Spokane, Washington, specializing in helping Christian couples with 401k five years from retirement.

- Fiduciary. No commission, no products

- Investment management and financial planning

More resources:

Schedule a meeting: Link

Monday morning outlook: Link